2025 CFA® Program Curriculum Changes ...

The CFA Program isn’t just evolving—it’s transforming. Every year, the CFA Institute fine-tunes... Read More

You are not chasing a job title.

You are chasing the right to make decisions with other people’s money.

And the moment you understand that, the question how to become a hedge fund manager stops sounding glamorous and starts becoming practical.

Because capital does not care about ambition.

It responds to judgment, repeatability and evidence.

Therefore, before anyone allows you to run risk, you must answer a silent test:

Why should we trust you?

Most articles stay vague here. They tell you to study finance, get internships and maybe earn a certification. Useful, yes, but far from sufficient.

What you really need is a map of how professionals move from curious beginners to trusted decision makers. You need to understand the hedge fund career path, what hiring managers screen for, how hedge fund interviews actually unfold and what separates someone who loves markets from someone who can manage money.

This article gives you that map.

We will talk honestly about the ladder from hedge fund analyst to portfolio manager. We will discuss strategy choices that shape your future. We will break down the skills you must build and the proof you must present. We will even cover the uncomfortable truths about pressure and job risk.

If you are serious about this career, clarity is your competitive advantage.

Let’s build it.

The phrase hedge fund manager is used loosely.

In practice, people usually mean the portfolio manager, the person with final authority over positions and risk.

The PM decides what enters the book, how large it becomes and when it leaves. Performance ultimately lands on their shoulders.

Research from places like Corporate Finance Institute consistently highlights that this responsibility is why the role is not entry-level. You grow into it through years of proven decision-making.

Where analysts fit

A hedge fund analyst generates ideas. They build financial models, test assumptions, track catalysts and recommend trades. Their work influences allocations but they are not the final owner of risk.

Where traders fit

Traders focus on execution. They obtain liquidity, manage transaction costs and help translate strategy into real positions.

Why this distinction matters for you

It matters because your preparation must match the seat you want one day.

If the destination is portfolio manager, then every stage of your development should move you closer to being trusted with independent judgment.

A realistic day in the life of a PM

Depending on the strategy, time may be spent:

Notice how little of that is classroom theory.

It is applied risk ownership.

Here is one of the biggest mistakes young candidates make.

They prepare generically.

But hedge funds are not generic. Strategy determines hiring profiles, interview formats and daily work.

Long Short Equity

You evaluate businesses, estimate intrinsic value and look for price dislocations. Deep accounting knowledge and narrative clarity are essential.

Global Macro

You interpret economic regimes, policy shifts and cross-asset relationships. Big picture thinking becomes critical.

Event Driven

You analyze corporate actions such as mergers or restructurings and assign probabilities to outcomes.

Relative Value and Arbitrage

You hunt for pricing inefficiencies between related securities.

Credit

You focus on balance sheet durability, covenants and recovery scenarios.

Quantitative and Systematic

Models, coding and data pipelines drive decisions, a path often emphasized by CQF Institute.

Discretionary vs quant daily reality

A discretionary analyst may spend hours reading filings, speaking with experts and refining valuation.

A quant researcher may spend the same hours cleaning data, refining algorithms and stress testing signals.

Different craft, same mission. Produce reliable returns.

Multi-manager vs single-manager platforms

In multi-manager environments, risk is tightly controlled and performance is evaluated quickly. Teams that underperform can be cut fast.

Single manager funds may allow longer horizons and broader autonomy.

Understanding this early helps you target the right employers.

Let’s remove mystery.

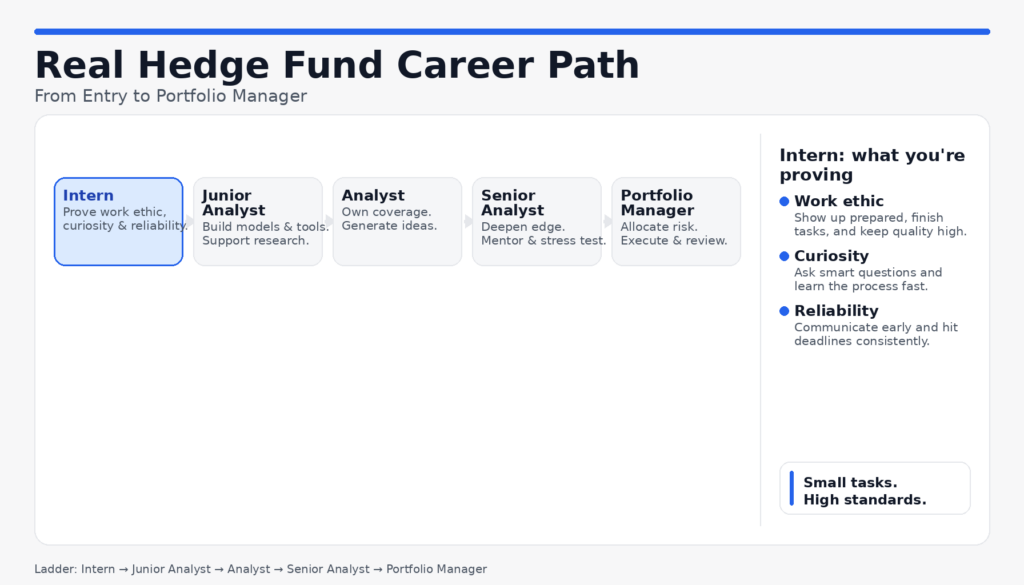

The ladder often looks like this, something described clearly by Mergers & Inquisitions.

Intern → Junior Analyst → Analyst → Senior Analyst → Portfolio Manager

The titles are simple. The expectations are not.

Intern

You prove work ethic, curiosity and reliability. Small tasks, high standards.

Junior analyst or research associate

You support senior staff. Data accuracy, speed and humility matter.

Analyst

Now you originate ideas. You defend them under pressure. Your accuracy starts affecting real money.

Senior analyst

Trust deepens. You influence sizing and mentor others. Your judgment begins to resemble that of a PM.

Portfolio manager

You own risk. You build the book. Results define your future.

Many professionals arrive via:

These backgrounds build analytical muscle before capital responsibility.

What if you lack elite brand names?

Then your evidence must be stronger.

Professionals have broken in through relentless cold outreach combined with exceptional stock pitches or data projects. When your proof of ability is undeniable, pedigree becomes less important.

Harder path. Absolutely possible.

Let’s drop buzzwords.

Hiring managers want to know if you can contribute tomorrow.

Discretionary investing skill set

You must show strength in:

If your memo is unclear, your idea is ignored.

Quant or systematic skill set

You will be evaluated on:

Messy methodology destroys credibility.

Here is the brutal truth.

Most candidates say they possess these abilities.

Very few can demonstrate them live.

Which brings us to the decisive advantage.

Imagine reviewing one hundred resumes.

Then one candidate sends:

Who receives the interview?

Exactly.

This is why experienced recruiters echo advice found on Mergers & Inquisitions. Demonstrated competence beats claimed interest.

A clear thesis.

Why mispricing exists.

Catalysts.

Downside risks.

Valuation framework.

Expected timeline.

Tight. Logical. Defensible.

What a strong quant package includes

Clean data.

Transparent assumptions.

Realistic transaction costs.

Robustness checks.

Professional, not academic.

Building the foundation

Serious mastery of investment analysis dramatically improves how fast you can construct these materials. The program from CFA Institute is respected because it strengthens valuation, ethics and portfolio thinking.

Many candidates use AnalystPrep resources to accelerate that understanding and translate theory into usable insight.

Preparation becomes output.

Unlike banks, hedge funds often hire when a need appears.

Processes are fluid. Timing is unpredictable.

As such, waiting for formal postings is dangerous.

Build a target list

Filter by strategy, size and geography. Know who fits your profile.

Study the fund

Read letters, public commentary and portfolio themes.

Make precise contact

Short introduction. Specific interest. Attach your proof of skill.

This approach shows seriousness.

Why smaller funds can be strategic

Mega funds attract oceans of applicants. Smaller operations may value initiative and differentiated thinking.

For candidates without traditional pedigrees, this can be a smarter entry.

Let’s handle this honestly.

No certification guarantees employment.

However, for discretionary tracks, the CFA charter strongly signals commitment to rigorous analysis and professional ethics.

For systematic paths, specialized quantitative training can be more relevant.

What matters is how credentials enhance your ability to produce investable ideas.

They open doors. They do not replace performance.

This environment rewards results.

Capital moves. Evaluations are constant. Underperformance has consequences.

Insights from Corporate Finance Institute underline the intensity of this performance culture.

Nevertheless, many professionals thrive precisely because the feedback loop is clear. Good decisions are rewarded. Weak ones are exposed quickly.

For driven personalities, that meritocracy is energizing.

How long does the hedge fund career path take?

For most professionals, the journey along the portfolio manager path takes a decade or more. Progress depends on the strength of your ideas, the trust you build with senior investors and how consistently you perform across different market environments.

Do you need the CFA to become a hedge fund manager or should you follow the CFA vs quant route?

It depends on which hedge fund strategies you want to work in. Fundamental and discretionary funds often value the analytical depth and ethics framework associated with the CFA program. Systematic or model driven teams may prioritize programming, statistics and research design. Neither route replaces the need to prove you can generate results, but each can strengthen your positioning for different seats.

What degree works best for hedge funds?

There is no single correct major. Finance and economics are common for discretionary roles, while mathematics, engineering and computer science are popular for the quant side. Ultimately, funds care about how effectively you can apply knowledge within real hedge fund strategies rather than what is printed on your diploma.

How do hedge fund interviews evaluate candidates?

Interviews are designed to test whether you are ready to move further along the portfolio manager path. Expect stock pitches, deep dives into your assumptions, modeling reviews and serious challenges to your risk thinking. Employers want evidence that you can survive in live decision environments.

What is the difference between a portfolio manager and a hedge fund manager?

In everyday conversation the terms are often interchangeable. Typically, the portfolio manager is the person who leads a strategy, allocates capital and bears responsibility for performance within a specific mandate or slice of the fund.

Becoming a hedge fund manager is not about collecting credentials or chasing prestige.

It is about gradually earning trust.

Trust from mentors. Trust from investors. Trust from teammates.

You earn it by demonstrating that your process is sound, your thinking is independent and your risk awareness is mature.

Build those qualities early. Document them. Present them confidently.

Do this consistently and the journey from hedge fund analyst to portfolio manager becomes not a fantasy but a professional progression.

Offered by AnalystPrep

The CFA Program isn’t just evolving—it’s transforming. Every year, the CFA Institute fine-tunes... Read More

The Executive Assessment is a requirement for admission to a growing number of... Read More

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.