Credit Risk Transfer Mechanisms

After completing this reading, you should be able to: Compare different types of... Read More

After completing this reading, you should be able to:

A financial crisis is a disruption of the capital markets that is occasioned by falling asset prices and insolvency of debtors and intermediaries. Such a disruption hurts the capacity of a market to allocate capital. Financial crises are often characterized by panic and bank runs during which investors either sell assets or withdraw funds from savings accounts. These actions are inspired by fears that the value of assets will decrease if they continue to be held in financial institutions. An economic crisis may also be caused by the burst of a speculative bubble, the crash of stock markets, sovereign default, or a currency crisis – a situation in which there’s a steep decline in the value of a nation’s currency. A financial crisis can be confined to a single economy, but it can also spread to an entire economy or even multiple economies around the world. There have been many crises in the last century, including the Great Depression in 1932, the Suez Crisis in 1956, the International Debt Crisis in 1982, the Russian Economic Crisis (1992-97), and the Latin American Debt Crisis in 1994-2002. However, none of these crises left as big a scar on the world’s economic landscape as the great financial crisis of 2007-2009, also referred to as the 2007/2009 financial crisis.

The 2007/2009 financial crisis was a period of general economic breakdown that affected not just the United States, where it began, but just about every country around the world. According to the International Monetary Fund (IMF), it was the worst crisis since the Great Depression in the 1930s. The 2007/2009 financial crisis is widely attributed to the collapse of the United States real estate market, particularly after the emergence of the subprime mortgage market.

The Great Financial Crisis of 2007-2009 (GFC) began in December 2007 and lasted for 19 months, until June 2009. Let’s look at some notable events that preceded the crisis.

Although conventional wisdom holds that the 2008 financial crisis was brought about by insufficient government monitoring of risk management in the private sector, there appears to be compelling evidence the true cause was the U.S. government’s housing policy. The government had passed legislation aimed at increasing homeownership by providing favorable mortgage terms to middle and lower-income earners. The government actively encouraged banks to extend mortgages to a broader borrower base in an attempt to bridge the gap between the poor and the middle class.

This ambitious policy was implemented primarily through the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, and the U.S. Department of Housing and Urban Development (HUD). Ultimately, the legislation forcefully relaxed traditional mortgage underwriting standards to make mortgage credit more readily available to lower-income borrowers. However, loosened standards spread across the wider market and contributed to an enormous house price bubble between 1997 and 2007. By 2008, most mortgages in the U.S. were subprime or weak and were failing at an unprecedented rate. The high default rate systematically weakened the financial markets, culminating in the failure of Lehman Brothers – one of the biggest investors in mortgage-backed securities.

A housing bubble is a temporary period of months or years during which housing prices are inflated beyond fundamentals due to high demand and low supply.

In the years leading up to the GFC, the U.S. economy was driven by a housing bubble. Home prices had consistently been increasing in the preceding years (2000 to 2007), although there were a few (insignificant) declines in between. The key reason behind this was the relative lax lending standards that rendered most Americans eligible for mortgages even when their creditworthiness wasn’t particularly impressive. When the bubble burst, financial institutions were left with trillions of dollars in subprime mortgage investments that were nearly worthless. In addition, housing construction fell by more than 4%, the national GDP tumbled, and consumption slowed.

The shadow banking system refers to the collection of non-bank financial intermediaries (NBFIs) providing services similar to those of traditional commercial banks but outside the normal regulatory framework for banks. In the years leading up to the GFC, the shadow banking system has recorded steady growth. Important NBFIs included securitization vehicles (SPVs), investment banks, money market funds, and mortgage companies. Due to inadequate regulation, the shadow banking system was marked by irrational exuberance and poor risk management. NBFIs were known to take higher liquidity and credit risk levels than traditional banks. The vast majority of NBFIs originated subprime mortgages, packaged them in mortgage-backed securities, and distributed them throughout the financial system. When it became clear the securitization market was headed for ruin, creditors ran from the shadow banking system, triggering a run that disrupted the flow of credit to consumers.

Due to the shadow banking system’s sheer size, interconnectedness with mainstream financial institutions, the complexity of operations and assets, and dependence on short-term funds, its failure had an enormous effect on the global financial system.

In the decades leading up to the GFC, households had been accumulating debt. When housing prices started falling, individuals and corporates concentrated on paying off debt while reducing consumption and investment. This gradually slowed down the economy.

The first prominent signs of problems manifested in early 2007 when Freddie Mac announced its decision to stop purchasing high-risk mortgages. Around the same time, New Century Financial, a leading mortgage lender to below-average-risk borrowers, filed for bankruptcy. In addition, credit rating agencies began to downgrade structured financial instruments.

Another sign that all was not well came when the ABX index – used as a benchmark for measuring the overall performance of the subprime mortgage market – began to reflect higher expectations of default. After these initial warnings, runs occurred in the short-term market (shadow banking system) – a market previously considered safe. Large-scale withdrawals from short-term funds were made. Issuers of asset-backed commercial papers started having difficulties rolling over their outstanding debt. What followed was a series of bankruptcy declarations and takeovers.

Countrywide Financial Corp. was a major U.S. mortgage lending company. The corporation was founded in the 1960s by Angelo R. Mozilo, a butcher’s son from the Bronx, and David Loeb, a founder of a mortgage banking firm in New York. Subprime lending provided Countrywide with a lot of benefits during the early 2000s. In 2001, mortgages accounted for 28 percent of Countrywide’s net income, with subprime loans raking in $280 million. By comparison, subprime loans had earned the corporation just $86.9 million in the previous year. In 2002, a significant and rapid increase occurred in Countrywide’s loan portfolios to minorities and low- to moderate-income households.

In 2007, Countrywide’s annual report took a somber tone after years of fast growth and optimistic projections. Countrywide had already begun to feel the effects of the financial crisis. The report focused a great deal on the accounting details of its mortgage portfolio and default rates. The report revealed that in just a year, Countrywide had depreciated over $20 billion and absorbed over $1 billion in losses. By 2008 there was approximately $8 billion worth of subprime loans in Countrywide’s books, and to make matters worse, the delinquency rate stood at 7% against an industry average of 4.67%. In the same year, foreclosures doubled, and the firm tried to cope with the situation by laying off around 20 percent of its employees (20,000 people). In 2008, the company was acquired by Bank of America after nearly failing due to a lack of funding. A substantial discount was applied to the price tag compared to what the company was actually worth. Shares had been valued at $20/share earlier in the year, but Bank of America paid just $8/share.

Bear Stearns was a global investment bank and financial company founded in 1923 in New York. It collapsed during the 2008 financial crisis.

Ahead of the collapse, Bear Stearns was heavily involved in securitization and issued large amounts of asset-backed securities. Even as investor losses mounted in those markets in 2006 and 2007, the company’s management felt it was a good time to increase exposure. To avert sudden collapse, the Federal Reserve Bank of New York provided an emergency loan in March 2008. Sadly, that wasn’t enough to save Bear Sterns. Unable to roll over its short-term funding, the bank was bought by JPMorgan Chase at a big discount. To put that into perspective, Bear Stern’s pre-crisis stock price stood at more than $130 a share, but JPMorgan was able to negotiate a price of just $10 a share.

In the mid-2000s, Lehman Brothers had massive exposure to mortgage-backed securities (MBS). The housing boom led to the creation of an unprecedented amount of MBSs and collateral debt obligations (CDOs). By 2007, Lehman Brothers was the largest holder of MBSs. But on September 15, 2008, Lehman Brothers filed for bankruptcy, marking the peak of the subprime mortgage crisis. But what exactly happened?

In the first two quarters of 2008, the bank reported losses running into billions of shillings due to the high default rate in the subprime mortgage business. Upon learning that Lehman had been downgraded due to these losses and heavy exposure to the mortgage industry, the Federal Reserve called Lehman to negotiate financing for its reorganization. After these discussions failed, Lehman filed a Chapter 11 petition. It remains the largest bankruptcy in American history. One day after the bankruptcy filing, the Dow Jones Industrial Average dropped by 4.5%, its biggest decline since September 11, 2001. This signaled the government’s limits in managing the crisis and consequently excited panic.

Lehman’s bankruptcy filing was a seismic event that shook the global financial system to the core. In the month following its collapse, equity markets lost more than $10 trillion in market capitalization.

The Reserve Primary Fund (RPF) was the first money market fund ever created in the U.S. During its peak, it held assets worth more than $60 billion. Amid the financial crisis of 2007-2008, RPF lost dollar value or “broke the buck.” “Breaking the buck” refers to a situation in which a money market fund’s investment income does not cover its operating expenses or investment losses. Eventually, RPF was liquidated. But the failure of Lehman Brothers had a very strong hand in the collapse of RPF.

RPF began to invest in commercial paper in 2006, an asset class the fund’s founder Bruce Bent had dismissed in 2001. By early 2008, 56% of the fund’s portfolio was comprised of asset-backed and financial-sector commercial paper. Lehman Brothers’ bankruptcy on September 15, 2008, raised concerns about RPF’s holdings of Lehman-issued paper, which, then, accounted for 1.2% of its portfolio. Among money market funds, RPF was especially vulnerable because it did not have a parent company that could guarantee its share price. Withdrawals from the fund clocked 25% by the afternoon of September 15 and more than half the following day. The withdrawals were motivated by clients’ decision to exit the fund before the price of its Lehman assets could impact RPF’s share price. Without a buyer, the fund declared the assets worthless and announced a $0.97 share price. The fund was liquidated at the end of September.

Subprime mortgages are mortgages given to individuals whose credit histories are poor, incomplete, or nonexistent. Subprime borrowers often have poor credit ratings, large loan-to-values (low up-front deposits), and high loan-to-income ratios. A typical subprime mortgage comes with a low “teaser” rate in the first couple of years which then reverts to a higher rate for the remaining term to maturity. In the years leading up to the GFC, subprime mortgages had several notable features:

Many subprime borrowers, some of whom were property speculators, were optimistic that at the end of their teaser period, they would be able to refinance to a similar or even better product or sell the homes at a profit. But when house prices declined, many of these borrowers found themselves in negative equity positions (the value of their mortgages exceeded the value of their homes). Many chose to default on their obligations, resulting in more foreclosures and a supply glut, further pushing house prices down.

The other notable practice in the lead-up to the financial crisis was the selling of loans to third parties under the OTD (originate-to-distribute) model. Under the model, lenders would issue mortgages to borrowers and then package them into secondary assets that could be sold to third-party investors. Prior to the sale, lenders would cease holding the mortgages as assets on their balance sheets. Instead, these loans would be moved into bankruptcy-remote structured investment vehicles (SIVs). Investors used to do business directly with the SIVs. In securitization, certain types of assets are bundled so that they can be repackaged into interest-bearing securities. Upon purchasing the securities, the purchasers receive interest and principal payments from the assets.

Collateralized debt obligations (CDOs) provide an example of such a structure, where the pool of securities is divided into multiple tranches (e.g., senior, junior, and equity). Cash flows and losses are shared according to a waterfall structure, where senior tranches receive cash flows first but absorb losses last. Despite the fact that the underlying mortgages consisted of NINJA and liar loans, the senior tranches were deemed very safe and had an AAA rating. At the same time, many of the junior tranches of multiple structures of CDOs were bundled and resold as CDO-squared (CDOs whose cash flows are backed by other CDO tranches rather than mortgages). In the end, some of the products developed from these structures were too complex and opaque to be valued, even during normal times and even for sophisticated investors.

The fact that CDOs created from NINJA loans and other substandard facilities were given an AAA rating demonstrates that rating agencies did very little to realistically and reliably assess the credit quality of the CDOs. Apparently, while conducting their credit analysis, rating agencies relied on data provided by issuers. In addition, rating agencies were usually paid by the issuer. In these circumstances, there was a clear conflict of interest because the arrangement gave rating agencies an incentive to issue favorable ratings. In other words, rating agencies were ready to turn a blind eye to possible underlying risks in exchange for huge “assessment fees” from issuers.

Banks were mainly originators of mortgage-backed securities. After successfully selling mortgages to consumers, banks securitize these mortgages (assets on the balance sheet) by creating structured investment vehicles (financial intermediaries) via which the pooled assets would be sold to investors. SIVs are usually designed to be bankruptcy-remote, meaning they have their own legal status. As a result, an SIV’s obligations are secure even if the parent company goes bankrupt. In the same breath, the operations of the S.P. are restricted to purchasing and financing specific assets or projects. These characteristics enabled banks to remove securitized assets from the balance sheet, a move that, in part, contributed to relaxed lending and know-your-customer (KYC) standards. As a result, the number of subprime mortgages would steadily increase as more and more assets got securitized.

Mortgage brokers serve as intermediaries, bringing together mortgage borrowers and lenders. Note, however, that they do not use their own funds to originate the loans.

Due to lax lending standards and weak internal controls, some brokers and borrowers submitted false documentation that allowed borrowers to obtain funding under fraudulent terms. The problem was exacerbated by the compensation structure for most mortgage brokers, which rewarded increasing the volume of loans originated while paying “lip service” to long-term performance. Brokers generally incurred few (if any) consequences if an originated loan eventually defaulted. As a result, they had little inspiration to perform proper due diligence.

During the Global Financial Crisis of 2008, credit agencies came under fire for giving high credit ratings to debts that later turned out to be high-risk investments. Specifically, they failed to identify (or overlooked) risks that might have warned investors against investing in certain instruments, such as mortgage-backed securities.

A potential conflict of interest between rating agencies and securities issuers was also highlighted. Rating agencies are paid by issuers of securities to provide rating services. As a result, they might be reluctant to assign very low ratings to the issuer’s securities.

An equally important point to note is that subprime mortgages were too new to provide reliable, proven data that could be used to draw long-term risk predictions. Therefore, many of the initial ratings assigned to these securitizations (most often the senior tranches with AAA ratings) were likely flawed from the start.

Short-term wholesale debt comprises two instruments: repurchase agreements (R.A.s) and commercial paper (C.P.).

Generally, a repurchase agreement (“repo”) is an agreement that involves the sale and subsequent repurchase of the same security at a higher price at a later date. It is a transaction in which a security is exchanged for cash. The security serves as collateral to the buyer until the seller can pay them back, and in addition, the buyer earns interest. Since the security seller receives cash at the beginning of the repo, the seller has the status of a borrower in a collateralized loan transaction (with the security as collateral). The security buyer, who provides cash at the beginning of the repo but receives a higher sum at the end of it, can be considered a lender (as the higher sum is equivalent to principal plus interest).

Repo transactions can use a variety of securities as collateral, from government bonds, highly rated corporate bonds, to securitized tranches. There is a direct relationship between the quality of collateral and the size of the haircut (that is, the difference between the initial market value of an asset and the purchase price paid for that asset at the start of a repo), with higher (lower) quality collateral having smaller (larger) haircuts. A haircut of 10% means that for every USD 100 pledged as collateral, a borrower can get USD 90. A haircut aims to protect a lender from having to sell collateral at a loss following a default and recovering less than the full amount of the loan. The bankruptcy process does not apply to repos. Consequently, if one counterparty fails, the other may unilaterally terminate the transaction and sell the collateral.

Unsecured CP financing involves issuing short-term debt that is not backed by any assets. Due to the absence of specific collateral that a lender can seize in the event of bankruptcy, unsecured commercial paper issuers typically have very high credit quality. Normally, if C.P. issuers’ credit quality deteriorates, for example, by way of a rating downgrade, an orderly exit will occur through margin calls.

However, there are special commercial papers that are backed by specific collateral. The collateral could be credit card loans, mortgages, or other securitizations. Such a commercial paper is known as an asset-backed commercial paper (ABCP).

SIVs holding mortgages were predominantly funded through ABCPs and repurchase agreements, so they had to roll over obligations at maturity to maintain liquidity. SIVs were, therefore, exposed to significant funding liquidity risk in the event of a crisis. As housing and mortgage-backed security prices declined, lenders began questioning the quality of the assets contained within SIV structures and they began extending fewer short-term loans. By August 2007, ABCP and repo markets had been shut down entirely. SIVs’ sponsors were also hurt since they often extended backstop lines of credit to these entities. The negative effect spread even further. For example, ACBPs had been popular investments for money market funds. When ABCP prices started tumbling, large-scale investors triggered financial hemorrhage among the leading money market funds by rushing to withdraw their stakes. This further exacerbated the liquidity crisis.

Systemic risk refers to the possibility that a company, or industrial-level event, could cause severe instability or even the collapse of an entire industry or economy.

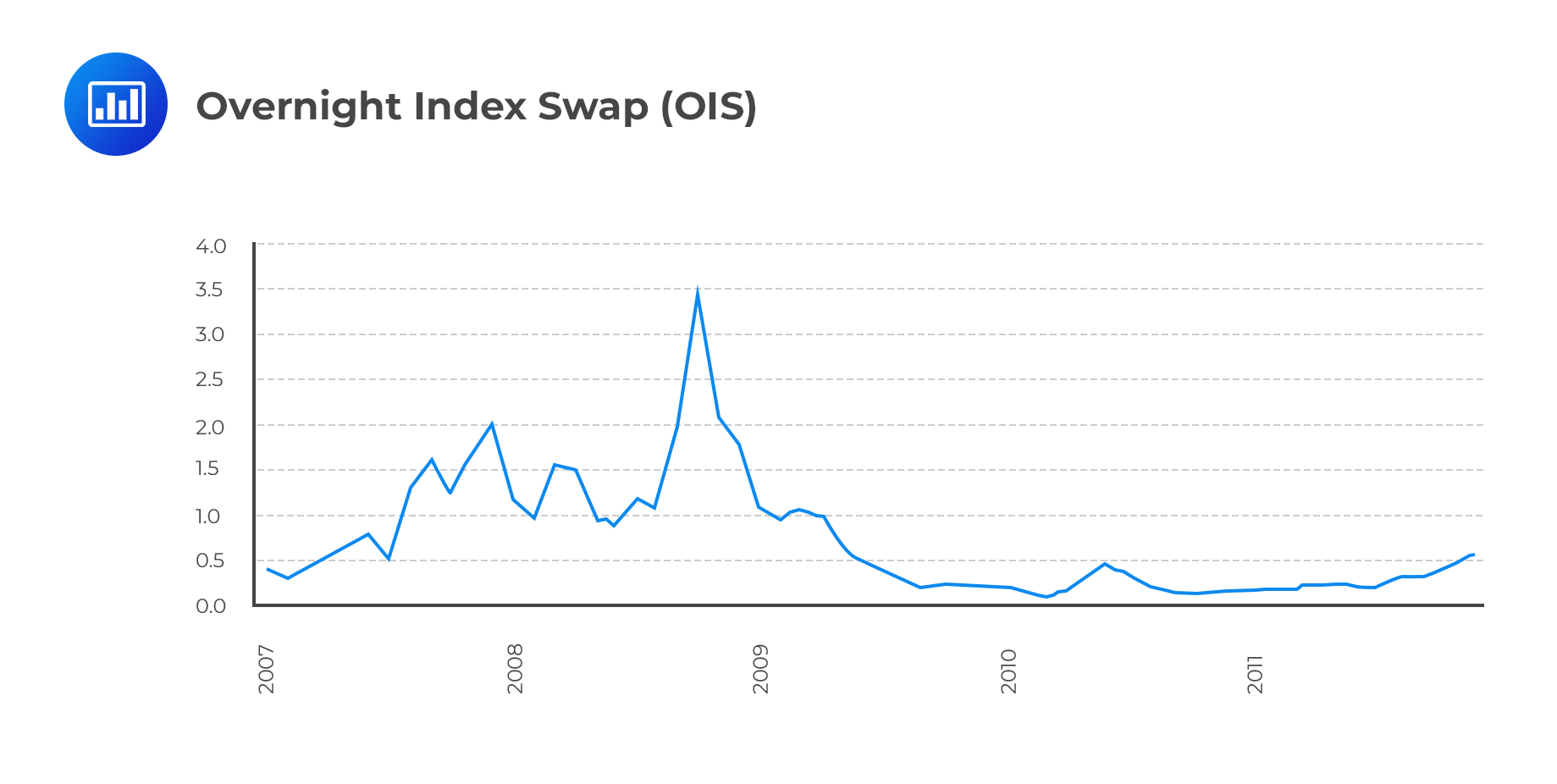

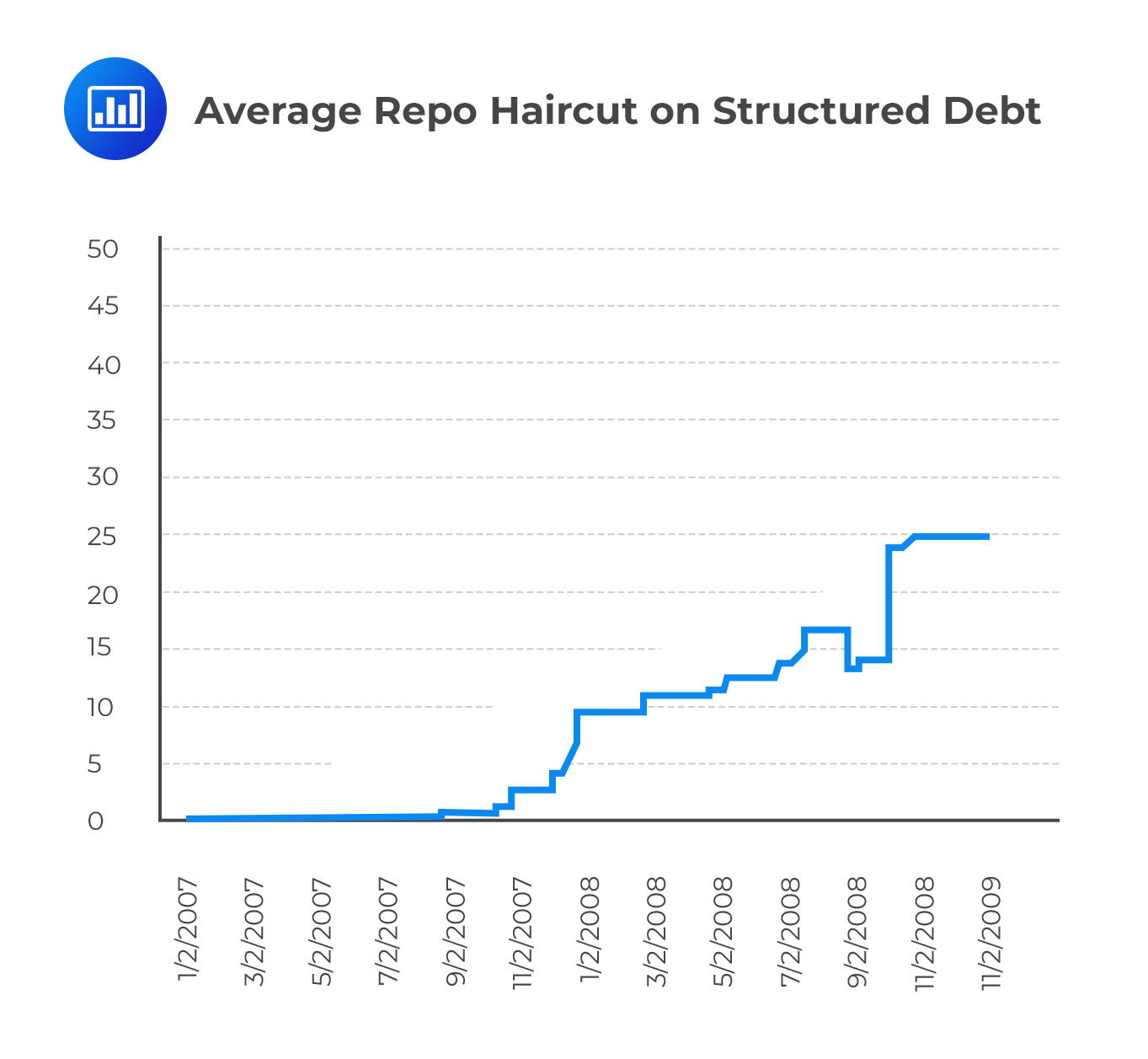

During the GFC, what began as a subprime mortgage crisis quickly escalated into a full-blown financial meltdown whose effects were felt across financial markets. Once market participants started to grow wary and weary of doing business with financial institutions with a direct or indirect stake in the mortgage industry, various actions were taken that ended up throwing financial markets further into turmoil. For example, haircuts on short-term funding increased from 0% before the crisis to nearly 25% in November 2008, shortly after the collapse of Lehman Brothers. The LIBOR-overnight index swap (OIS) spread, one of the most trusted indicators of the overall health of the financial system, shot up from nearly 0% pre-crisis to over 3.6% at the peak of the crisis. The sharp increase pointed to dwindling confidence among participants in the interbank lending market. At the same time, some institutions that could not borrow in the short-term market were left with no choice but to sell some of their assets in distress. This further pushed market prices down and left these institutions with “bare bone” equity levels that couldn’t support long-term/strategic objectives. Consequently, some filed for bankruptcy, while a few lucky ones were either bailed out by the government or absorbed by other relatively stable institutions.

To combat the crisis, the Federal Reserve and other central banks from around the world devised innovative liquidity injection facilities. The Federal Reserve created backstop facilities to support most asset classes that experienced stress during the crisis. These actions included:

These actions aimed at improving liquidity. This led to central banks’ balance sheets becoming significantly larger.

U.S. government interventions during the crisis were as follows:

Question

In the lead-up to the U.S. subprime mortgage crisis from 2007 to 2009, a sharp increase in delinquency rates was noted starting in mid-2005. As a risk management specialist, you are analyzing the factors that may have contributed to this trend. Which of the following accurately identifies a circumstance that likely exacerbated the rise in subprime mortgage delinquencies during that period?

A. The level of over-collateralization for mortgage-backed securities surged in 2005, providing increased risk mitigation.

B. The Federal Reserve implemented a series of substantial interest rate cuts in 2005, reducing the cost of borrowing.

C. Lenders aggressively promoted zero down payment mortgage products to first-time and subprime buyers in 2005.

D. Housing prices began to rise sharply towards the end of 2005.

Solution

The correct answer is C.

During the buildup to the subprime mortgage crisis, many financial institutions and lenders were offering mortgages to individuals who were often not qualified to repay them. One characteristic of this problem was the offering of loans with low or zero down payments. These risky loans were given to subprime borrowers who might not have the financial stability to manage the mortgage, especially if interest rates were to rise or if housing prices were to fall.

Option A is incorrect as over-collateralization would generally be seen as reducing risk, not increasing it.

Option B is incorrect because rising interest rates, not falling, would typically lead to higher delinquency rates, especially among subprime borrowers with adjustable-rate mortgages.

Option D is incorrect because rising housing prices would tend to decrease delinquencies, as homeowners would have more equity in their homes, making them less likely to default on their loans.

Offered by AnalystPrep

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.