Risk-Return Characteristics

When the underlying share price is well below the conversion price, the convertible... Read More

The following steps should be followed when calibrating binomial interest rate trees to match a particular term structure:

When constructing an interest rate tree as per step 2 above, it’s important to remember that:

The following related formulas are important to remember:

$$i_{1,u}=i_{1,d}e^{2\sigma }$$

$$i_{2,uu}=i_{2,dd}e^{4\sigma }$$

$$i_{2,uu}=i_{2,du}e^{2\sigma }$$

$$i_{2,du}=i_{2,dd}e^{2\sigma }$$

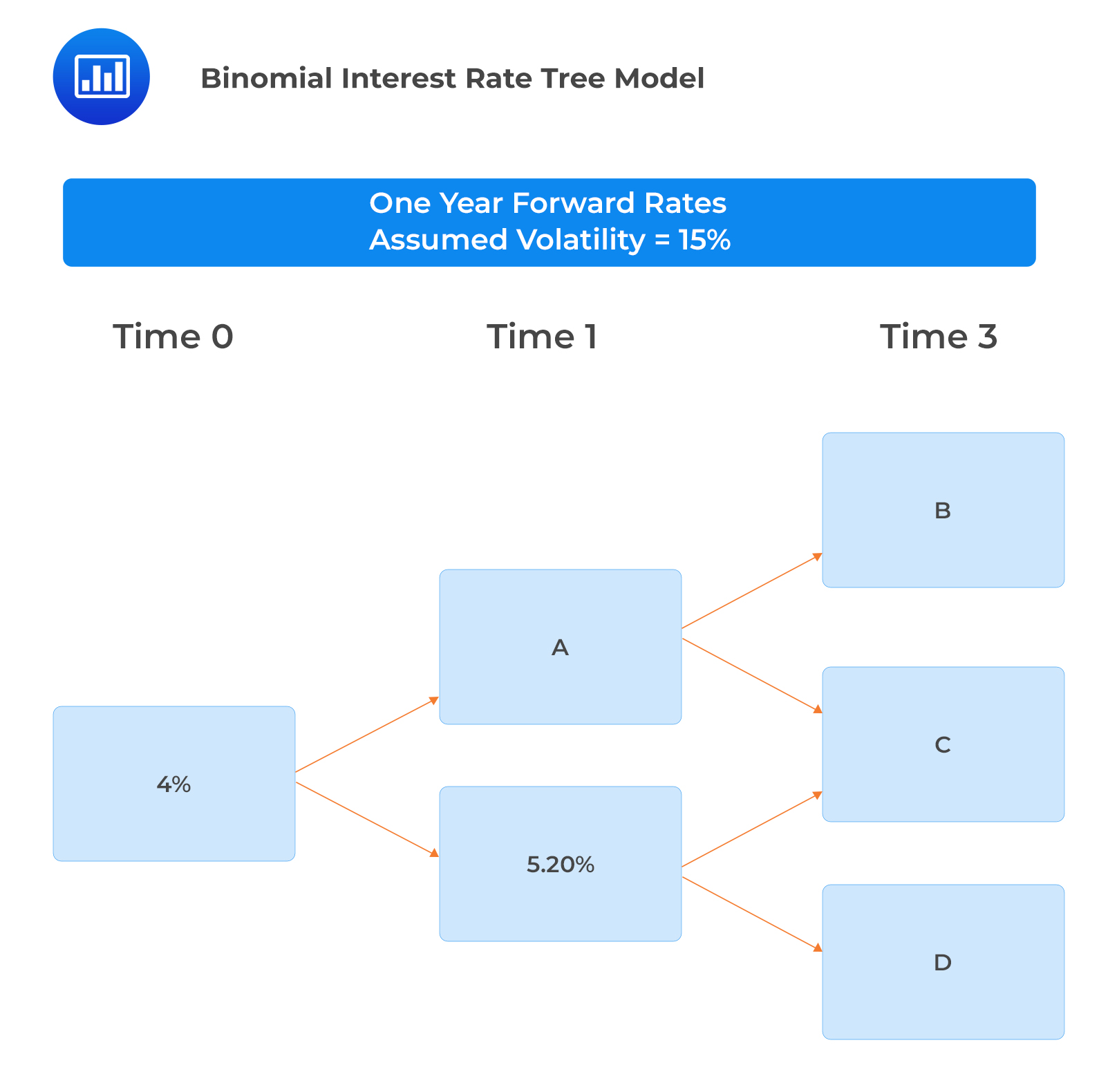

To calibrate a binomial interest rate tree, a portfolio manager collects the following information relating to the spot rate curve and forward rates:

$$ \begin{array}{c|c} \textbf{Term to Maturity} & \textbf{Spot Rate} \\ \hline 1 & 4.00\% \\ \hline 2 & 5.00\% \\ \hline 3 & 6.00\% \end{array} $$

Determine the forward rates A, B, C, and D.

Determine the forward rates A, B, C, and D.

Forward rate A

$$ \begin{align*} \text{The higher rate is determined as } i_{1u}&=i_{1d}\times e^{2\sigma} \\ &=5.20\%\times e^{2\times0.15}=7.019\% \end{align*} $$

Forward rate C

This is the middle forward rate approximated as \(f (2,1)\). Recall from the previous reading the relationship between forward and spot rates:

$$ \begin{align*} \left[1+f\left(t,T-t\right)\right]^{T-t} &=\left[\frac{\left(1+S_T\right)^T}{\left(1+S_t\right)^t}\right] \\ (1+f\left(2,1\right) &=\left[\frac{\left(1+S_3\right)^3}{\left(1+S_2\right)^2}\right] \\ f\left(2,1\right) &=\frac{{1.06}^3}{{1.05}^2}-1=8.029\% \end{align*} $$

Forward rate B

$$ \begin{align*} i_{2,uu} &=i_{2du } e^{2\sigma} \\ i_{2,uu} &=8.029\%\times e^{2\times0.15 }=10.84\% \end{align*} $$

Forward rate D

$$ \begin{align*} i_{2,dd} &=i_{2du} e^{-2\sigma} \\ i_{2,dd} &=8.029\%\times e^{-2\times0.15 }=5.95\% \end{align*} $$

It is key to note that the change in the volatility assumption affects implied forward rates. A change of volatility to a lower value makes the potential implied forward rates to collapse on the tree and vice versa.

Question

Chen Cheng, a portfolio manager at ABC Investment Bank, is training Zhang Wang, a junior investment analyst, on calibrating binomial interest rate models using Excel. Cheng starts the process by guessing a lower one-year forward rate, \(i_{1,d}\), of 3.820%. Assuming that Cheng uses a volatility assumption of 20%, the higher one-year forward rate using the lognormal model of interest rates is closest to:

- 2.56%.

- 4.67%.

- 5.70%.

Solution

The correct answer is C.

Based on the lognormal model of interest rates, the higher one-year forward rate is \((i_{1,u})=i_{1,d}e^{2\sigma}\).

$$ \begin{align*} i_{1,d} &=3.820\% \\ (i_{1,u}) &=3.820\%\times e^{2\times0.20}=5.70\% \end{align*} $$

Reading 29: The Arbitrage-Free Valuation Framework

LOS 29 (d) Describe the process of calibrating a binomial interest rate tree to match a specific term structure.

Offered by AnalystPrep

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.