Assume that we have samples of size \(n\) for dependent variable \(Y\) and independent variable \(X\). We wish to estimate the simple regression of \(Y\) and \(X\). The classic normal linear regression model assumptions are as follows:

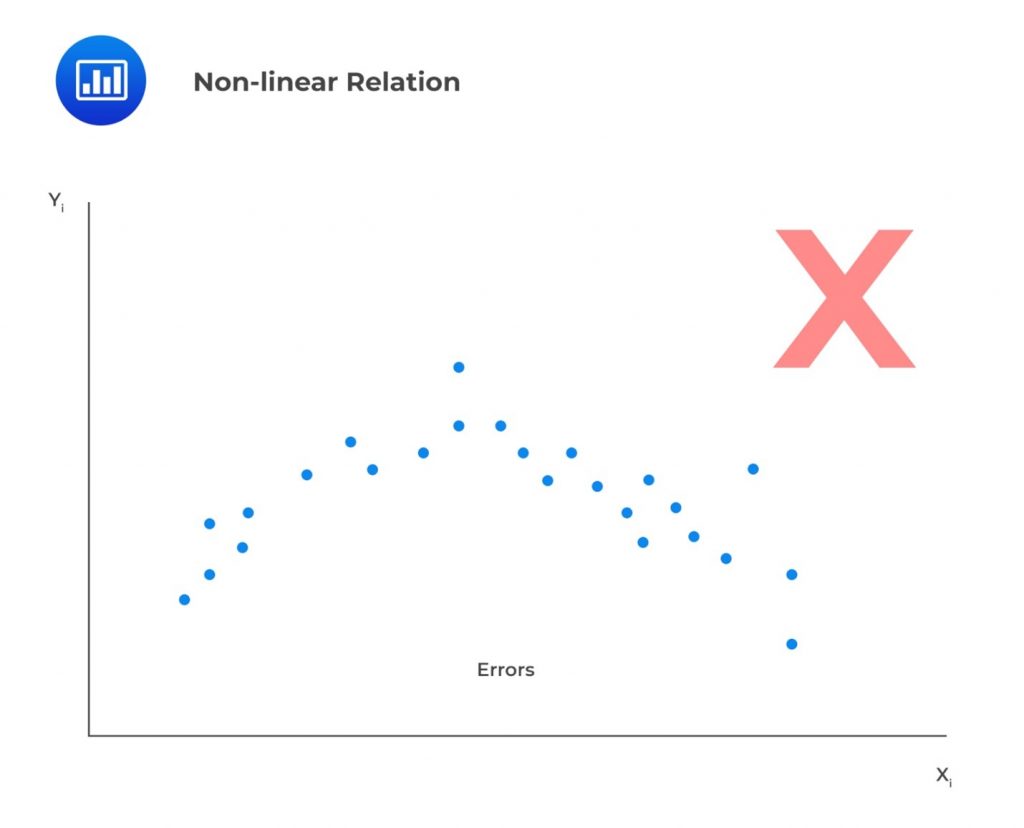

Linearity: A linear relationship implies that the change in \(Y\) due to a one-unit change in \(X\) is constant, regardless of the value \(X\) takes. If the relationship between the two is not linear, the regression model will not accurately capture the trend, resulting in inaccurate predictions. The model will be biased and underestimate or overestimate \(Y\) at various points. For example, the model \(Y=b_0+b_1e^{b_1x}\) is nonlinear in \(b_1\). For this reason, we should not attempt to fit a linear model between \(X\) and \(Y\). It also follows that the independent variable, \(X\), must be non-stochastic (must not be random). A random independent variable rules out a linear relationship between the dependent and independent variables. In addition, linearity means the residuals should not exhibit an observable pattern when plotted against the independent variable. Instead, they should be completely random. In the example below, we’re looking at a scenario where the residuals appear to show a pattern when plotted against the independent variable, \(X\). This effectively indicates a nonlinear relation.

Normality Assumption: This assumption implies that the error terms (residuals) must follow a normal distribution. It’s important to note that this doesn’t mean the dependent and independent variables must be normally distributed. However, checking the distribution of the dependent and independent variables is crucial to identify any outliers. A histogram of the residuals can be used to detect if the error term is normally distributed. A symmetric bell-shaped histogram indicates that the normality assumption is likely to be true.

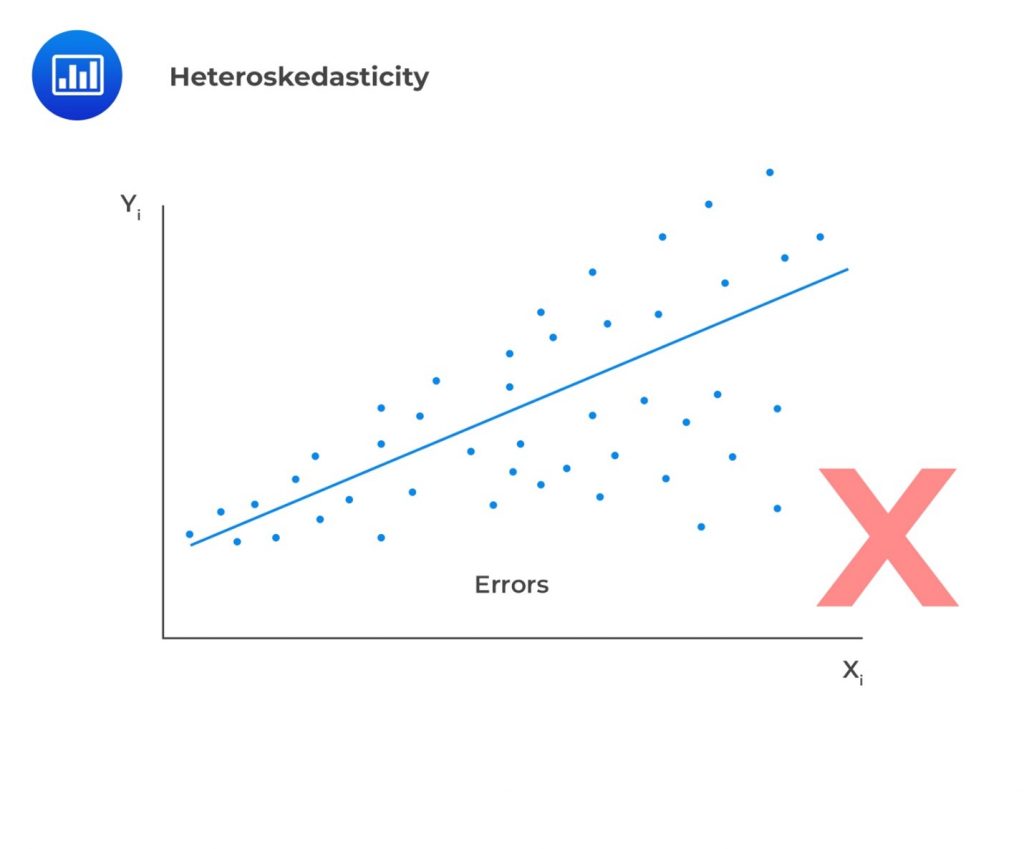

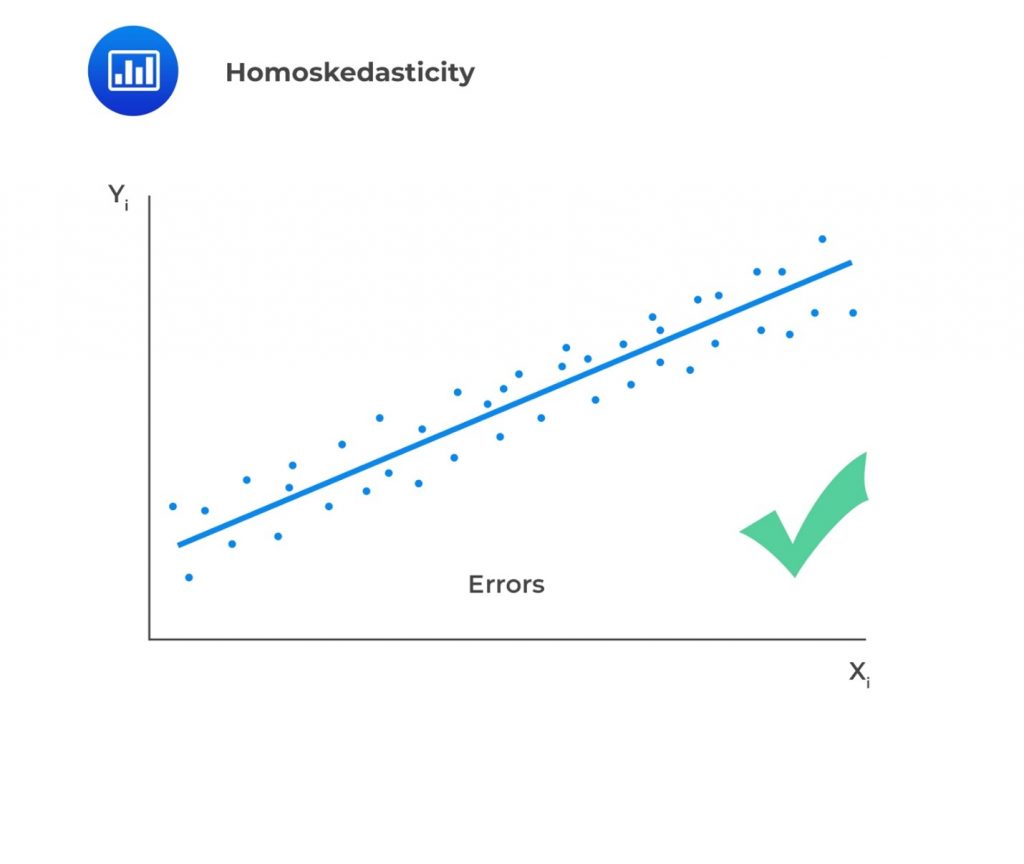

Homoskedasticity: Homoskedasticity implies that the variance of the error terms is constant across all observations. Mathematically, this is expressed as:$$ E\left(\epsilon_i^2\right)=\sigma_\epsilon^2,\ \ i=1,2,\ldots,n $$If the variance of residuals varies across observations, then we refer to this as heteroskedasticity (not homoscedasticity). We plot the least square residuals against the independent variable to test for heteroscedasticity. If there is an evident pattern in the plot, that is a manifestation of heteroskedasticity. In case residuals and the predicted values increase simultaneously, then such a situation is known as heteroscedasticity (or heteroskedasticity).

Independence Assumption: The independence assumption implies that the observations \(X_i\) and \(Y_i\) are independent of each other. Failure to satisfy this assumption implies the variables are not independent, and thus, residuals will be correlated. To ascertain this assumption, we visually and statistically analyze the residuals to check whether residual shows exhibit a pattern.

Question

A regression model with one independent variable requires several assumptions for valid conclusions. Which of the following statements most likely violates those assumptions?

The independent variable is random.

The error term is distributed normally.

There exists a linear relationship between the dependent variable and the independent variable.

Solution

The correct answer is A.

Linear regression assumes that the independent variable, X, is NOT random. This ensures that the model produces the correct estimates of the regression coefficients.

B is incorrect. The assumption that the error term is distributed normally allows us to easily test a particular hypothesis about a linear regression model.

C is incorrect. Essentially, the assumption that the dependent and independent variables have a linear relationship is the key to a valid linear regression. If the parameters of the dependent and independent variables are not linear, then the estimation of that relation can yield invalid results.

Access CFA Level I quantitative methods study notes, practice questions, mock exams, and video lessons to strengthen your understanding of the assumptions underlying linear regression.

Excelente para el FRM 2

Escribo esta revisión en español para los hispanohablantes, soy de Bolivia, y utilicé

AnalystPrep para dudas y consultas sobre mi preparación para el FRM nivel 2 (lo tomé una sola vez y aprobé muy bien), siempre tuve un soporte claro, directo y rápido, el material sale rápido cuando hay cambios en el temario de GARP, y los ejercicios y exámenes son muy útiles para practicar.

diana

2021-07-17

So helpful. I have been using the videos to prepare for the CFA Level II exam. The videos signpost the reading contents, explain the concepts and provide additional context for specific concepts.

The fun light-hearted analogies are also a welcome break to some very dry content.

I usually watch the videos before going into more in-depth reading and they are a good way to avoid being overwhelmed by the sheer volume of content when you look at the readings.

Kriti Dhawan

2021-07-16

A great curriculum provider. James sir explains the concept so well that rather than memorising it, you tend to intuitively understand and absorb them.

Thank you ! Grateful I saw this at the right time for my CFA prep.

nikhil kumar

2021-06-28

Very well explained and gives a great insight about topics in a very short time. Glad to have found Professor Forjan's lectures.

Marwan

2021-06-22

Great support throughout the course by the team, did not feel neglected

Benjamin anonymous

2021-05-10

I loved using AnalystPrep for FRM.

QBank is huge, videos are great.

Would recommend to a friend

Daniel Glyn

2021-03-24

I have finished my FRM1 thanks to AnalystPrep. And now using AnalystPrep for my FRM2 preparation. Professor Forjan is brilliant. He gives such good explanations and analogies. And more than anything makes learning fun. A big thank you to Analystprep and Professor Forjan. 5 stars all the way!

michael walshe

2021-03-18

Professor James' videos are excellent for understanding the underlying theories behind financial engineering / financial analysis. The AnalystPrep videos were better than any of the others that I searched through on YouTube for providing a clear explanation of some concepts, such as Portfolio theory, CAPM, and Arbitrage Pricing theory. Watching these cleared up many of the unclarities I had in my head. Highly recommended.

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.

In case residuals and the predicted values increase simultaneously, then such a situation is known as heteroscedasticity (or heteroskedasticity).

In case residuals and the predicted values increase simultaneously, then such a situation is known as heteroscedasticity (or heteroskedasticity).