Climate Change: Physical Risk and Equity

After completing this reading, you should be able to: From the perspective of... Read More

After completing this reading, you should be able to:

The Basel framework is part of a raft of measures that have been introduced following high-impact financial crises in recent years. The overall goal is to strengthen the banking system and avoid systemic vulnerabilities.

The initial phase of the Basel III framework was announced in 2010. It focused on the following objectives:

The Basel III reforms announced in 2017 sought to complement the initial phase of the Basel III reforms. In particular, they sought to restore credibility in the calculation of risk-weighted assets and improve the comparability of ratios across banks:

Credit risk is undoubtedly the biggest source of risk for banks. As such, it contributes towards a significant part of regulatory capital requirements put in place. The committee’s improved standardized approach for credit risk seeks to:

Under the IRB approach, banks are allowed to use their internal rating systems conditional on approval by their supervisors. Banks can use:

The main motivation behind changes to the credit risk IRB approach is to introduce similar capital requirements that enhance comparability across banks and address lack of robustness in modeling certain asset classes.

The main changes include the following:

In the most recent global financial crisis (2007/2008), banks suffered huge losses resulting from CVA risk – losses related to the deterioration of a counterparty’s creditworthiness in derivative contracts. In the aftermath of the crisis, the committee enhanced the CVA framework. Objectives include:

In addition, banks with minimal engagement activities in derivative transactions can use their credit counterparty risk (CCR) capital requirements as a proxy for their CVA charge. A bank whose centrally cleared derivatives are worth EUR 100 billion or less may calculate its CVA capital charge as a simple multiplier of its counterparty CCR charge.

The operational risk capital requirement can be summarised as follows:

$$ \text{Operational risk capital} = BIC \times ILM $$

We seek to now further define each term from the equation.

$$ \text{Business Indicator Component} = \left( BIC \right) =\sum { \left( { a }_{ i }\times { BI }_{ i } \right) } $$

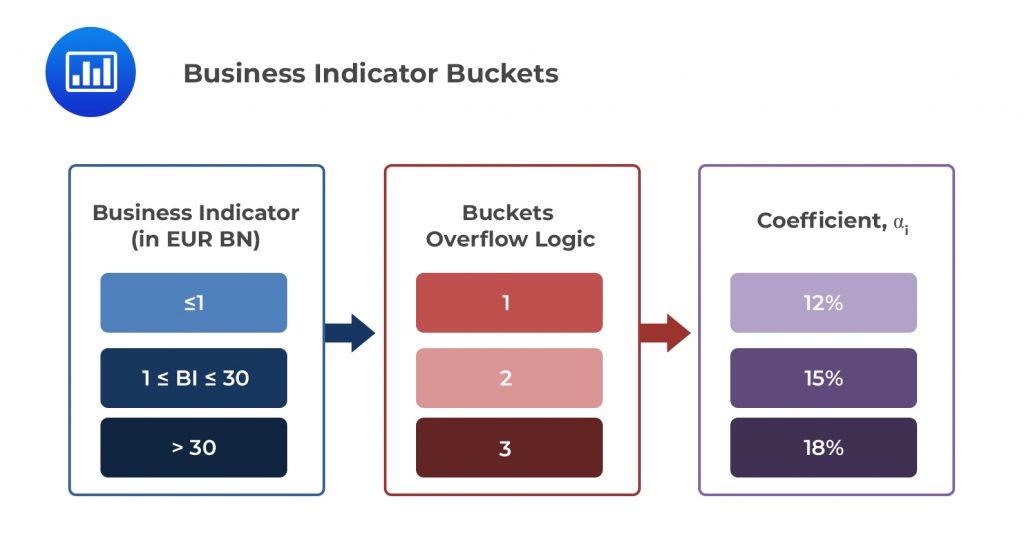

The Bl (Business Indicator) is the sum of three components:

The business indicator is a set of marginal coefficients multiplied by the Bl based on three buckets (where i = 1, 2, 3 denotes the buckets). As the business indicator expands (in € billion), the coefficient applied becomes larger. The buckets are summarized in the table below:

Example 1: Calculating the BIC of a Bank With a BI of €50bn.

Example 1: Calculating the BIC of a Bank With a BI of €50bn.$$

\small{\begin{array}{l|c|c|c}

\textbf{BI Bucket}& \textbf{1} & \textbf{2}& \textbf{3} \\ \hline

\textbf{BI Range} & ≤ €1 \text{ billion} & €1 \text{ billion} < BI ≤ €30 \text{ billion} & ≥€30 \text{ billion} \\ \hline

\textbf{Marginal BI Coefficient, } \bf{{ a }_{ i }} & 0.12 & 0.15 & 0.18 \\ \hline

\textbf{Calculation} \bf{{ a }_{ i }} & €1bn × 12\%

= €0.12bn & €(30 – 1) × 15\% = €4.35bn & €(50 – 30) × 18\%= €3.6bn \\

\end{array}}

$$

By summing the 3 buckets, we arrive at a BIC of €8.07 billion.

The Internal Loss Multiplier is a function of the BIC and the Loss Component (LC), where the latter is equal to 15 times a bank’s average historical losses over the preceding 10 years. It is noteworthy that firms with less than 20 years of data must use a minimum of 5 years of data.

The leverage ratio is a complement to the risk-weighted capital requirement and prevents a situation where banks take on unsustainable levels of debt. To mitigate the externalities or, rather, the ripple effect associated with the failure of G-SIBs, the leverage ratio is set at 50% of a G-SIB’s risk-weighted higher-loss absorbency requirements. For example, a G-SIB subject to a 4% risk-weighted higher-loss absorbency requirement would be subject to a 2% leverage ratio buffer requirement.

Capital distribution constraints are imposed on entities that do not meet the leverage ratio requirement.

The Basel III reforms set a floor in capital requirements calculated under internal models at 72.5% of those required under standardized approaches. Due to the potential impact of the floor, the 72.5% requirement is expected to be implemented in phases over a five-year period from 2020 to 2026.

When calculating the floor, banks will be expected to take the following risks into account:

Practice Question

Which of the following changes has Basel III set forth with reference to the changes in credit risk?

- New exposure classes and evaluation tools have been introduced.

- Definitions within the internal ratings-based approach (IRB) have been aligned to those under the standardized approach.

- Retail exposures have been aggregated to simplify the analytical process.

- Introduction of further due diligence requirements to limit reliance on external credit rating.

A. All of the above.

B. I, III, and IV.

C. II and III.

D. I, II, and IV.

The correct answer is: D).

III is incorrect. A more granular treatment applies to retial exposures. This is the distinction between different types of retail exposures.

Offered by AnalystPrep

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.