Active Share Versus Active Risk

Active Share Active Share represents the degree to which the underlying portfolio mimics... Read More

The approach to managing currency risk in a portfolio varies widely among participants. Some choose not to take action, believing that long-run returns will eventually mean- revert. On the other end of the spectrum, some participants see an active management opportunity. This is informed by their belief that markets are not entirely efficient.

Do Nothing Full Speculation [] []

In real-world scenarios, currency management is subject to various constraints that influence investors’ approach. These constraints can vary widely, encompassing factors such as stakeholders’ attitudes and the availability of capital, ultimately shaping the strategies employed to manage currency risk.

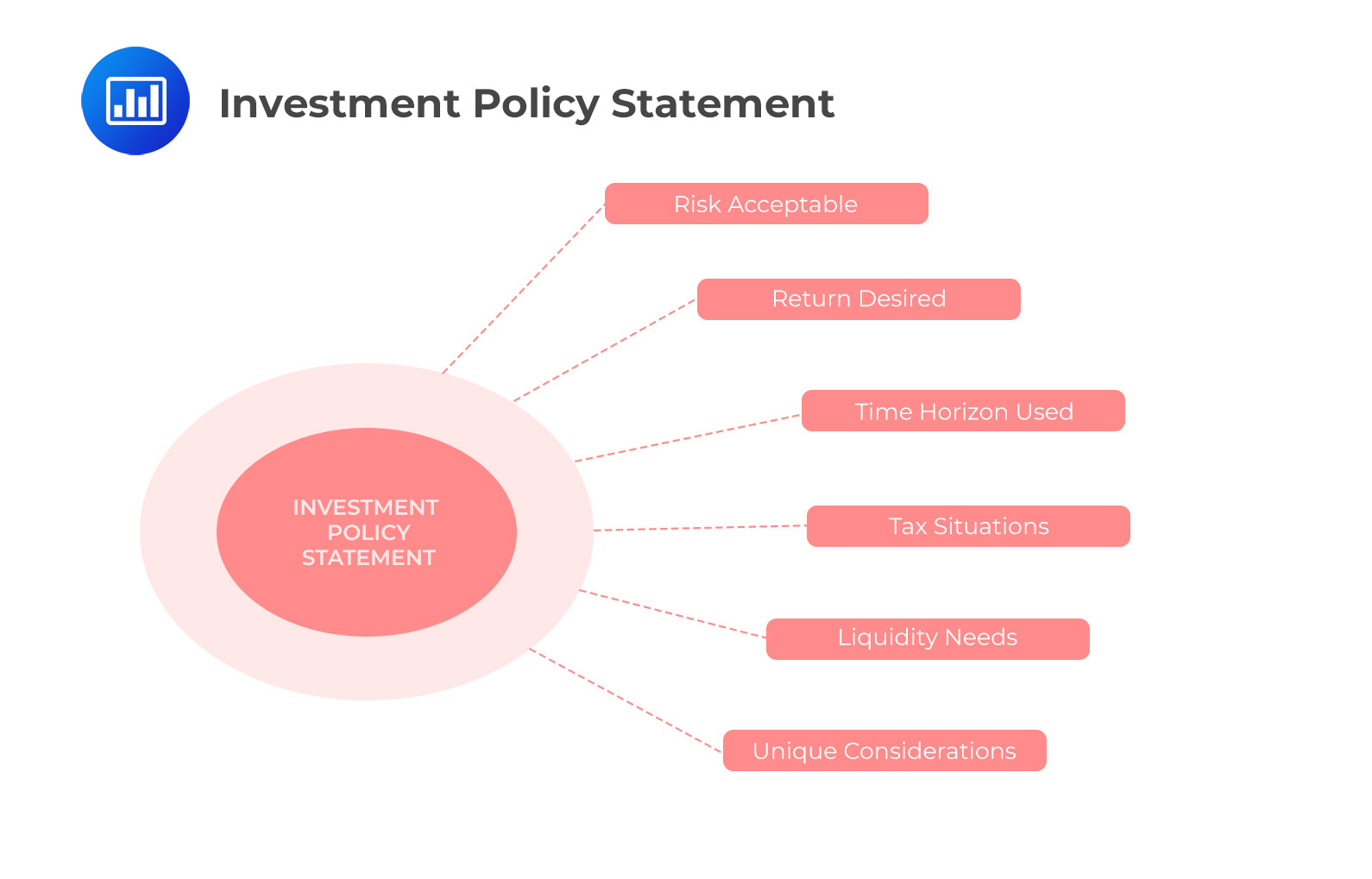

The first place to look for real-world constraints in managing portfolio currency risk is the Investment Policy Statement (IPS). The IPS plays a crucial role in guiding decisions related to hedging currency risk. It includes specific sections that address various aspects of currency risk management, such as:

The IPS (Investment Policy Statement) plays a crucial role in quantitatively defining how currency risk will be managed in the portfolio. This is typically articulated through various factors, including:

Calculating an efficient frontier for a multi-currency portfolio can be challenging due to the need for multiple opinions on expected risks, returns, and correlations of currency pairs. To simplify the process, real-world practice typically breaks it down into two steps.

In the first step, the portfolio manager selects the portfolio weights (ωi) for the foreign-currency assets that optimize the expected risk-return trade-off of the foreign-currency assets, assuming no currency risk.

In the second step, the portfolio manager determines the desired currency exposures for the portfolio and decides how far to relax the constraint to achieve a full currency hedge for each pair.

As shown previously, the formulas for currency portfolio expected risk and return are used to quantify the expectations and create a mean-variance efficient portfolio.

Two key themes emerge when deciding how to manage currency risk in a portfolio: time horizon and portfolio composition.

Time horizon plays a significant role in determining the extent to which currency risk should be hedged. Some proponents of the “doing nothing” approach believe that currencies will mean-revert to their long-run values due to interest rate and exchange rate parities preventing arbitrage. However, the duration over which currencies may deviate from their long-run no-arbitrage prices can be much longer than most investors are willing to endure, possibly spanning decades. An impatient investment committee may lead to a shift from a passive “do-nothing” approach to an active currency management style.

Portfolio composition refers to the asset classes in which the underlying foreign currencies are invested. Portfolios with exposure to fixed-income assets often exhibit a greater desire to hedge currency risk. This is because fixed income and currencies tend to fluctuate similarly in response to interest rate movements. In such cases, managers of fixed-income portfolios may choose to hedge the currency risk to avoid waiting for two sources of return to drop simultaneously. On the other hand, equities are more influenced by changes in expected earnings rather than interest rates. This makes equity portfolios less likely to be fully hedged than fixed-income ones.

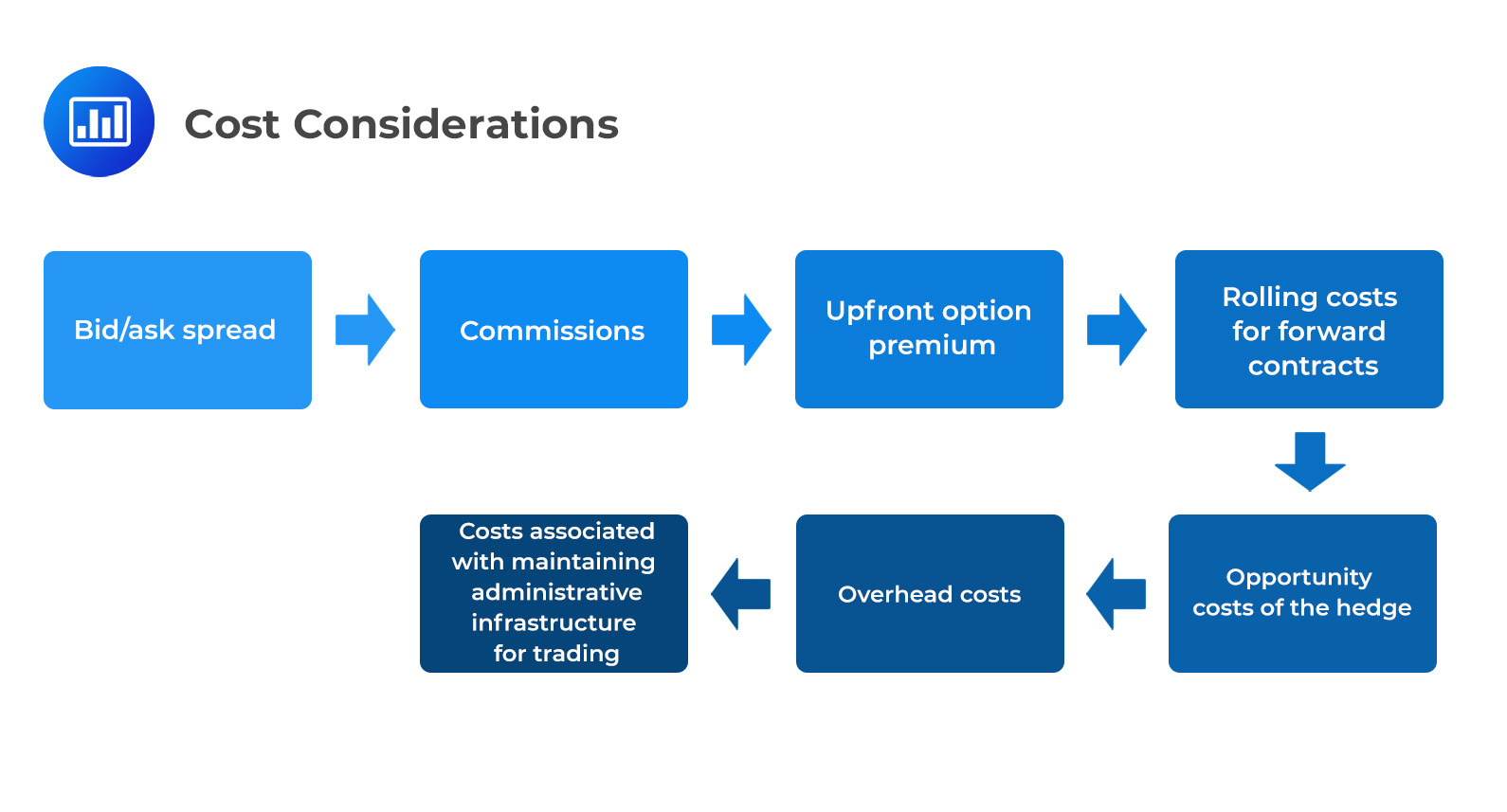

Hedges, much like insurance products, come with costs. Those who advocate for the no-hedge approach often emphasize these associated expenses. When initiating a currency hedging program, various costs may be involved, including:

Opportunity costs are an essential consideration in currency hedging strategies as they arise from the possibility of missing out on favorable currency movements. These costs represent the potential gains that could have been realized if the currency had been left unhedged and appreciated. When deciding whether to implement a currency hedge, investors must carefully weigh the benefits of risk reduction against the opportunity costs associated with potentially forgoing favorable currency fluctuations.

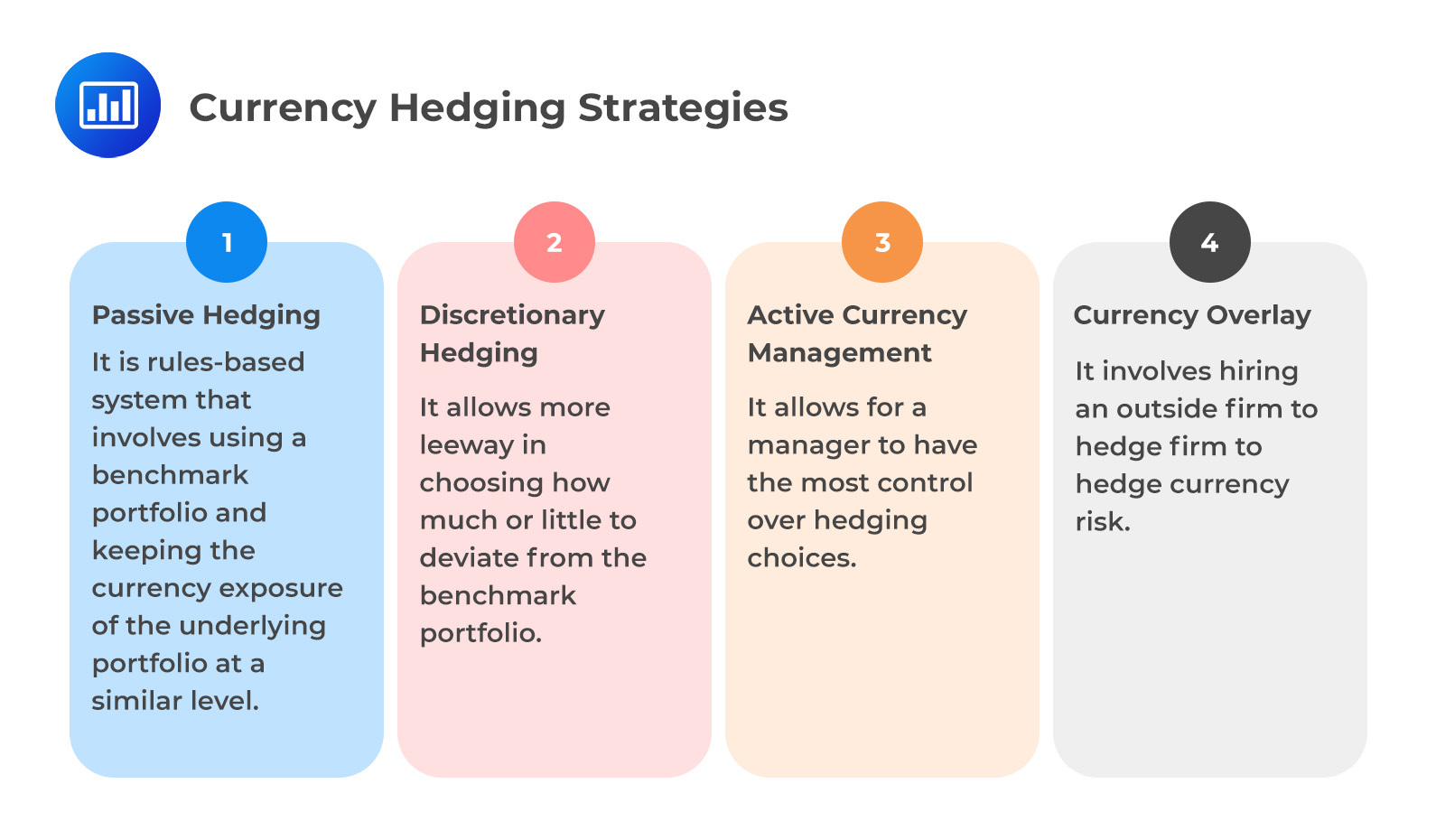

Passive hedging is an approach used to manage currency risk in a portfolio. It entails matching the currency exposure of the underlying assets to that of a specified benchmark portfolio. The objective is to keep the currency exposure aligned with the benchmark without actively making decisions based on market views or forecasts. The approach is rules-based. If the currency exposure deviates from the benchmark beyond a pre-determined threshold, the portfolio is rebalanced to align it with the benchmark. This strategy aims to replicate the benchmark’s currency exposure. It may involve periodic adjustments to maintain the desired level of hedging.

Discretionary hedging is an extension of the passive hedging approach. It grants a portfolio managers greater flexibility in deciding how much they may deviate from the benchmark portfolio.

Active currency management extends beyond discretionary hedging, giving portfolio managers greater control over hedging decisions. Managers can express directional biases and engage in currency speculation to potentially enhance portfolio returns. However, even in highly discretionary portfolios, there are usually some minimum constraints on management decisions to prevent significant losses.

Currency overlay is a strategy that involves outsourcing the task of hedging currency risk to an external firm. This approach is often considered beneficial when the external firm specializes in managing currency risk and related decisions. The outside consultants are given a considerable level of flexibility, and this approach is generally categorized as active management.

Summary of Strategies:

Question

Which of the following is least likely an argument favoring a passive-hedging strategy?

- A portfolio has an infinite time horizon.

- A portfolio consists mainly of fixed-income securities.

- Neither of the above is correct.

Solution

The correct answer is A.

Passive hedging is positioned on one end of the spectrum, advocating for stringent controls over currency risk. In this approach, stakeholders typically view currency risk as detrimental to the portfolio and believe that hedging is not overly expensive.

A portfolio with an infinite time horizon, such as many foundations, may be managed by stakeholders who believe that currency prices tend to revert to their long-run values over time. They may argue against implementing tight hedge controls, as they expect the currency risk to naturally correct over the extended lifespan of the portfolio.

B is incorrect. A portfolio heavily invested in fixed-income securities is more likely to be hedged against currency risk. This is because currency and fixed income often exhibit similar risk characteristics, making hedging a more practical strategy to manage currency fluctuations in such portfolios.

Reading 3: Currency Management: An Introduction

Los 3 (b) Discuss strategic choices in currency management

Strengthen your ability to evaluate currency risk decisions under real-world portfolio constraints.

Offered by AnalystPrep

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.