Model Training

Machine learning (ML) model training entails three tasks: method selection, performance evaluation, and... Read More

The term structure is a relationship between interest rates and maturities of similar quality bonds. A yield curve is a graphical representation of the term structure of interest rates.

The following theories explain the term structure of interest rates and the shape of the yield curve:

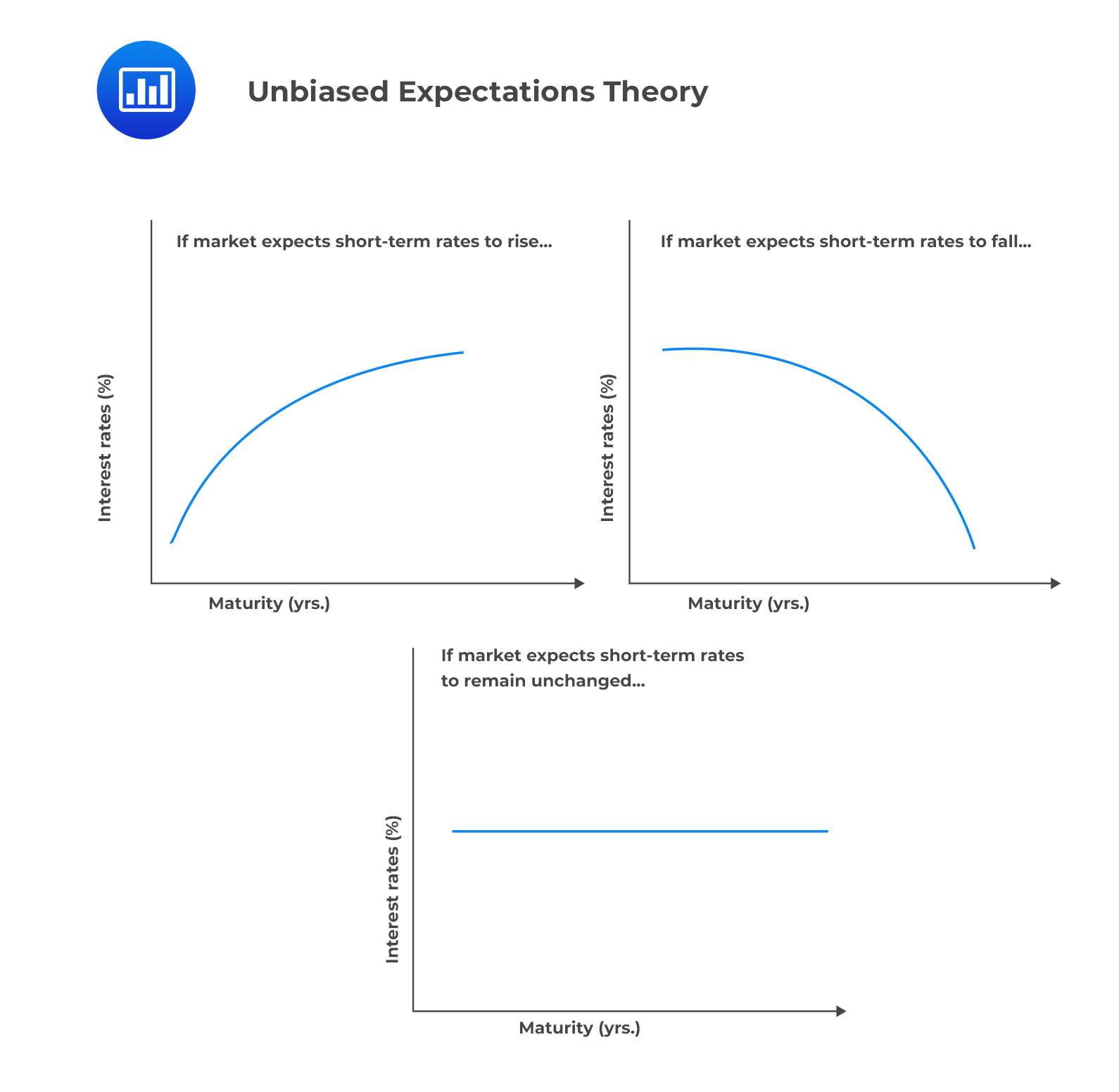

The unbiased expectations theory states that every maturity strategy leads to the same expected returns over a given investment horizon. This theory implies that the yield curve is impacted only by the market expectation of future interest rates.

The long-maturity rates will be higher than short-maturity rates (upward sloping yield curve) if the market expects interest rates to rise. The opposite is true if the market expects interest rates to fall. Moreover, a flat yield curve implies that the interest rates are not expected to change in the future.

This theory assumes that investors are not affected by uncertainty and that risk premiums do not exist. This is referred to as risk neutrality.

Local Expectations Theory

Local Expectations TheoryThe local expectations theory is a narrower interpretation of the unbiased expectations theory, which asserts that the expected return on bonds with varying maturities is the same only over short-term periods. This is based on the no-arbitrage condition.

For example, if an investor buys two similar bonds, one that matures in six years and another matures in 12 years. According to the local expectations theory, the two bonds will generate equal returns over a short-term period.

This theory suggests that long-term investors are not compensated for the reinvestment rate risk or interest rate risk.

The liquidity preference theory suggests that lenders prefer to lend short term while borrowers prefer to borrow long term. This makes the forward rates higher than expected future spot rates.

Thus, investors require a liquidity premium as a reward for lending long-term bonds. Further, these premiums increase with maturity. This theory predicts an upward sloping yield curve.

Preferred habitat theory (PHT) is similar to the market segmentation theory, as it holds that lenders and borrowers strongly prefer particular maturities based on their objectives.

The only variation under PHT is that investors will seek different maturities to their preferred ones, i.e., their usual habitat, if the expected extra returns are large enough for them.

Suppose longer-term debt has significantly high enough expected returns relative to the short-term debt. In that case, lenders will buy long-term debt even though investing in long-term debt is associated with higher risks.

Similarly, suppose the short-term rates are significantly lower than the long-term rates. In that case, lenders will issue more short-term bonds to take advantage of the lower rates against their preference for longer maturities to match their expected income streams.

The market segmentation theory suggests that different market participants have different maturity preferences. For example, pension funds are interested in longer-term rates, market makers focus on short-term rates, and businesses’ objectives point to medium-term rates.

These agents are either unable or unwilling to make any other investment, which is not in line with their maturity preference. The rates are determined by the supply and demand for long-term and short-term debts for the different market segments.

Question

The theory that suggests that the shape of the yield curve reflects the expectation about future short-term rates is most likely:

- Unbiased expectations theory.

- Local expectations theory.

- Preferred Habitat Theory.

Solution

The correct answer is A.

The unbiased expectations theory argues that the forward rate is an unbiased predictor of the future spot rate. It suggests that the shape of the yield curve reflects the expectation about future short-term rates.

B is incorrect. The local expectations theory is a narrower interpretation of the pure expectations’ theory, which asserts that the expected return will be the same over a short-term horizon starting today.

C is incorrect. The preferred habitat theory (PHT) argues that lenders and borrowers strongly prefer specific maturities based on their investment objectives

Additionally, investors will seek different maturities to their preferred ones, i.e., their usual habitat, if the expected extra returns are large enough for them.

Reading 28: The Term Structure and Interest Rate Dynamics

LOS 28 (h) Explain traditional theories of the term structure of interest rates and describe each theory’s implications for forward rates and the shape of the yield curve.

Practice term structure theories, yield curve analysis, forward rate interpretation, and fixed-income valuation concepts with CFA Level II study notes, practice questions, video lessons, and mock exams.

Offered by AnalystPrep

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.