Calculating and Interpreting Measures ...

Measures of dispersion are used to describe the variability or spread in a... Read More

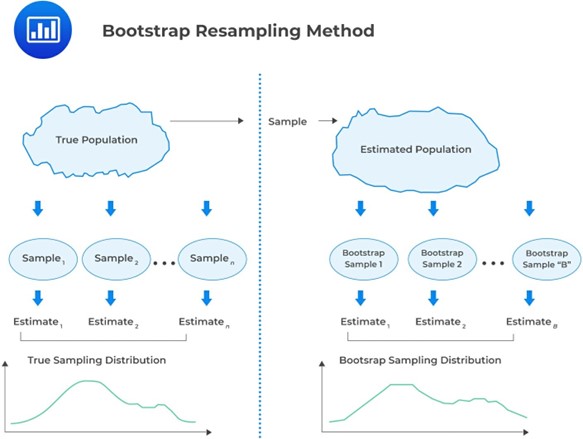

Resampling refers to the act of repeatedly drawing samples from the original observed data sample for the statistical inference of population parameters. The two commonly used methods of resampling are bootstrap and jackknife.

Using a computer, the bootstrap resampling method simulates drawing multiple random samples from the original sample. Each resample is the same size as the original sample. These resamples are used to create a sampling distribution.

In the bootstrap method, the number of repeated samples drawn is at the researcher’s discretion. Note that bootstrap resampling is done with replacement.

Furthermore, we can calculate the standard error of the sample mean. This is done by resampling and calculating the mean of each sample. The following formula is used to estimate the standard error.

$$ s_{\bar{X}}=\sqrt{\frac{1}{B-1}\sum_{b=1}^{{B}}\left({\hat{\theta}}_b-\bar{\theta}\right)^2} $$

Where:

\(s_{\bar{X}}\) = Estimate of the standard error of the sample mean.

\(B\) = Number of resamples drawn from the original sample.

\({\hat{\theta}}_b\) = Mean of a resample.

\(\bar{\theta}\)= Mean across all the resample means.

The bootstrap resampling method can also be used to estimate the confidence intervals for statistics on other population parameters, such as the median.

Jackknife is a resampling method in which samples are drawn by omitting one observation at a time from the original data sample. This process involves drawing samples without replacement. For a sample size of \(n\), we need \(n\) repeated samples. This method can be used to reduce the bias of an estimator or to estimate the standard error and the confidence interval of an estimator.

Question

Assume that you are studying the median height of 100 students in a university. You draw a sample of 1000 students and obtain 1000 median heights. The mean across all resample means is 5.8. The sum of squares of the differences between each sample mean, and the mean across all resample means \(\sum_{b=1}^{{B}}\left({\hat{\theta}}_b-\bar{\theta}\right)^2\) is 2.3.

The Estimate of the standard error of the sample mean is closest to:

- 0.05.

- 0.08.

- 0.10.

Solution

The correct answer is A.

$$ \begin{align*}

s_{\bar{X}}&=\sqrt{\frac{1}{B-1}\sum_{b=1}^{{B}}\left({\hat{\theta}}_b-\bar{\theta}\right)^2} \\

&=\sqrt{\frac{1}{1000-1}\times 2.3}=0.04798\approx 0.05

\end{align*} $$

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.