Capital allocation describes the process companies use to make decisions on capital projects, i.e., projects with a lifespan of one year or more. It is a cost-benefit exercise that seeks to produce results and benefits which are greater than the costs of the capital allocation efforts.

There are several steps involved in the capital allocation process. However, the specificity of the procedures a manager adopts depends on factors such as the manager’s position in the company, the size and complexity of the project being evaluated, and the company’s size.

The typical steps involved in the capital allocation process are:

Idea generation: Generating good ideas is the most important step.

Investment analysis: Information is gathered, which helps forecast cash flows for each project and evaluate a project’s profitability.

Capital allocation planning: This involves looking at project timing, scheduling, prioritizing, and coordinating.

Monitoring and post-audit: How a project performs is assessed, and actual results (revenues, expenses, cash flows, etc.) are compared with planned or projected results.

Capital Allocation Principles

Decisions are based on cash flows: Decisions are made based on cash flows rather than accounting or accrual basis (net income or operating income), which subtracts non-cash expenses such as depreciation.

Measure incremental cash flows: These are the additional cash flows that result from an investment.

Timing of cash flows is crucial: These are the predicted cash flows’ anticipated timing, length, volatility, and likelihood.

Cash flows are analyzed on an after-tax basis: Decisions should reflect the impact of taxes.

Cash flows are not accounting net income or operating income: Unlike accounting income, economic income (cash inflows + changes in a company’s market value) does not account for non-cash expenses.

Financing costs are ignored: Financing expenses can be ignored in cash flows since they are considered when calculating the required rate of return.

The “required rate of return” is the rate used to discount the cash flows disregarding financing expenses. Given a project’s riskiness, the needed rate of return is the discount rate that the issuer’s capital providers want. This discount rate is also known as the “cost of capital” or the “opportunity cost of money.” Based on its average-risk investment and the capital sources used to fund its assets, a company’s weighted average cost of capital (WACC) is its cost of capital at the enterprise level.

Capital Allocation Concepts

Sunk costs: These are costs that have already been incurred.

Incremental cash flow: This is the cash flow that is realized because of a decision made.

Externality: This refers to the effect of an investment on other things besides itself. If possible, these effects should be part of an investment decision. Cannibalization is one example of an externality. This occurs when an investment results in customers and sales moving away from a subsidiary of a company.

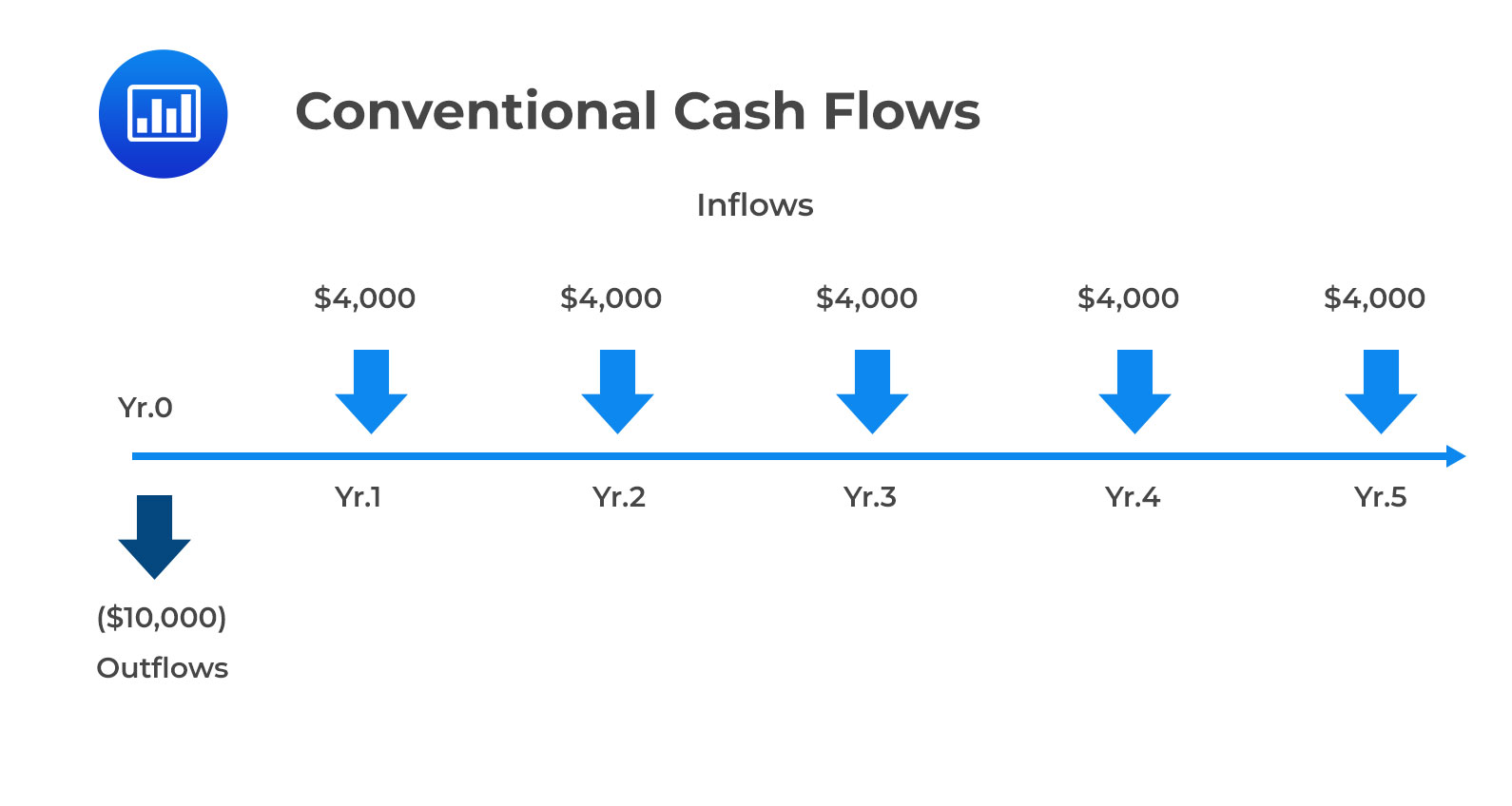

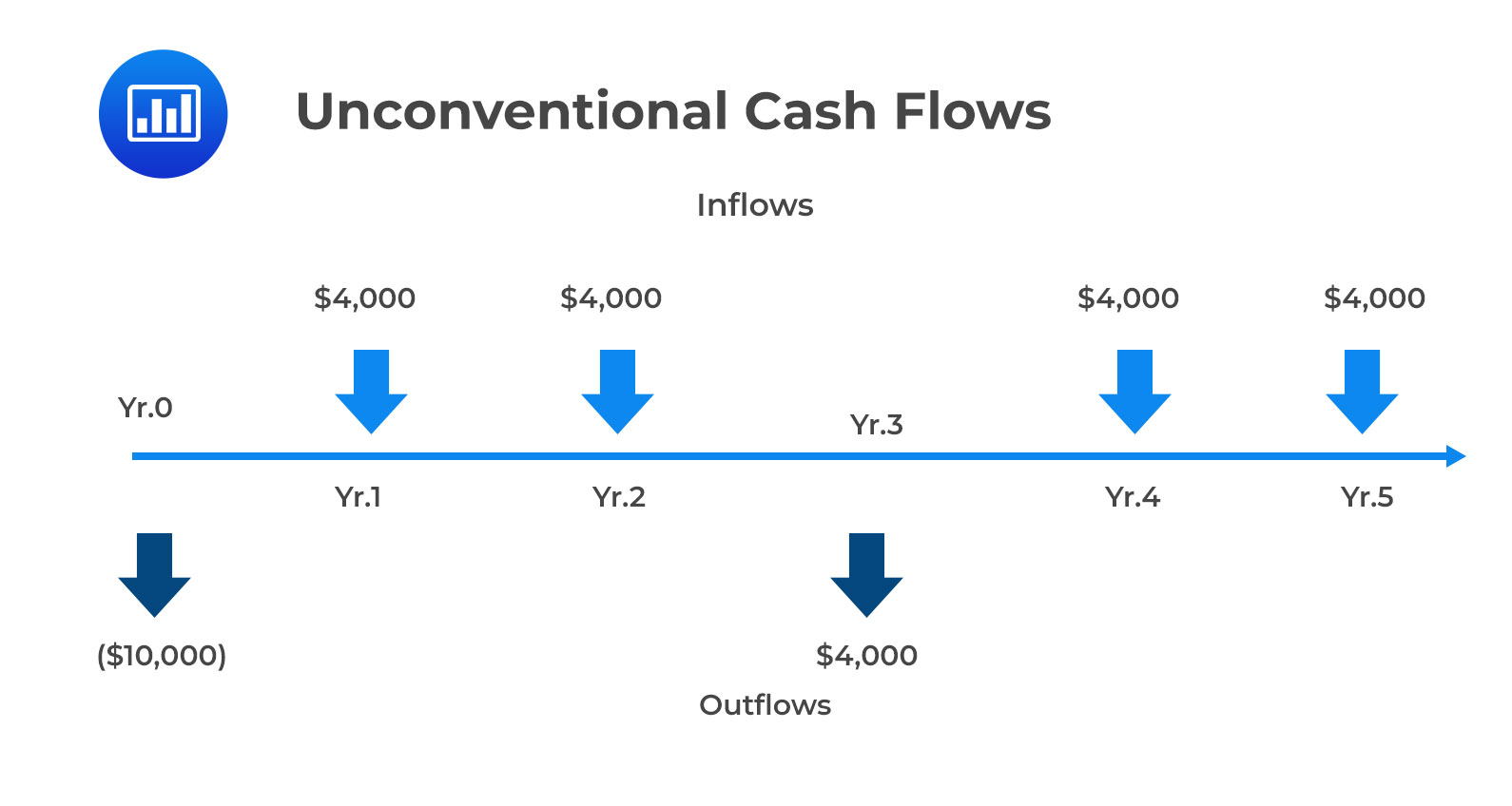

Conventional cash flows versus non-conventional cash flows: A conventional cash flow pattern has an initial cash outflow followed by a series of cash inflows. Conversely, a non-conventional cash flow pattern is one in which the initial cash outflow is not followed by cash inflows only. The cash flows can shift from positive to negative, again (or even change signs several times).

Independent Projects versus Mutually Exclusive Projects

Mutually exclusive projects are capital projects which compete directly against each other. For example, if a manager has projects X and Y and must choose either of the two and not both, then projects X and Y are said to be mutually exclusive. This scenario differs from independent projects, those whose cash flows are independent of each other and can, therefore, be undertaken together.

Project Sequencing

Project sequencing aims to arrange projects in a logical order for completion. It enables a project manager to determine the order of project completion. Indeed, project sequencing best manages the available time and resources.

Through project sequencing, investing in one project may create the option to invest in future projects. For example, a manager may invest in one project today and then invest in another project in a year. This happens if the financial results of the first project or new economic conditions are favorable.

Question

Which of the following statements is most likely accurate?

In capital allocation, only pre-tax cash flows should be considered.

The timing of cash flows is crucial to the capital allocation process.

A non-conventional cash flow pattern has an initial cash outflow followed by a series of cash inflows.

The correct answer is B.

Capital allocation analysts make an extraordinary effort to detail precisely when cash flows occur.

A is incorrect. Cash flows are analyzed after-tax; taxes must be fully reflected in capital allocation decisions.

C is incorrect. A conventional cash flow pattern (not a non-conventional cash flow pattern) has an initial cash outflow followed by a series of cash inflows.

Practice capital budgeting and allocation questions—incremental vs sunk costs, after-tax cash flows, cash-flow timing, and discount rates (WACC/required return)—with full CFA®-style solutions.

Excelente para el FRM 2

Escribo esta revisión en español para los hispanohablantes, soy de Bolivia, y utilicé

AnalystPrep para dudas y consultas sobre mi preparación para el FRM nivel 2 (lo tomé una sola vez y aprobé muy bien), siempre tuve un soporte claro, directo y rápido, el material sale rápido cuando hay cambios en el temario de GARP, y los ejercicios y exámenes son muy útiles para practicar.

diana

2021-07-17

So helpful. I have been using the videos to prepare for the CFA Level II exam. The videos signpost the reading contents, explain the concepts and provide additional context for specific concepts.

The fun light-hearted analogies are also a welcome break to some very dry content.

I usually watch the videos before going into more in-depth reading and they are a good way to avoid being overwhelmed by the sheer volume of content when you look at the readings.

Kriti Dhawan

2021-07-16

A great curriculum provider. James sir explains the concept so well that rather than memorising it, you tend to intuitively understand and absorb them.

Thank you ! Grateful I saw this at the right time for my CFA prep.

nikhil kumar

2021-06-28

Very well explained and gives a great insight about topics in a very short time. Glad to have found Professor Forjan's lectures.

Marwan

2021-06-22

Great support throughout the course by the team, did not feel neglected

Benjamin anonymous

2021-05-10

I loved using AnalystPrep for FRM.

QBank is huge, videos are great.

Would recommend to a friend

Daniel Glyn

2021-03-24

I have finished my FRM1 thanks to AnalystPrep. And now using AnalystPrep for my FRM2 preparation. Professor Forjan is brilliant. He gives such good explanations and analogies. And more than anything makes learning fun. A big thank you to Analystprep and Professor Forjan. 5 stars all the way!

michael walshe

2021-03-18

Professor James' videos are excellent for understanding the underlying theories behind financial engineering / financial analysis. The AnalystPrep videos were better than any of the others that I searched through on YouTube for providing a clear explanation of some concepts, such as Portfolio theory, CAPM, and Arbitrage Pricing theory. Watching these cleared up many of the unclarities I had in my head. Highly recommended.

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.