The Best Study Strategies for CFA® Ca ...

Can You Really Pass the CFA Exam While Working Full Time? Are you... Read More

Bond valuation is an application of discounted cash flow analysis. The general approach to bond valuation is to utilize a series of spot rates to reflect the timing of future cash flows.

Value can be described as the demand or the utility for money, whereas price is the amount of money to be paid.

Therefore, time-value-of-money is a concept that relates to the worth of money to time. It is used by investors in the market to understand that the present value of money is worth more than the same amount in the future.

In computations, what is calculated is the value. The price is not calculated but is determined by the demand and supply forces. Whereas price is the same for everyone, the value differs from person to person.

For option-free or fixed rate bonds, future cash flows are a series of coupon interest payments and a repayment of principal at maturity. The price of the bond at issuance is the present value of future cash flows discounted at the market discount rate.

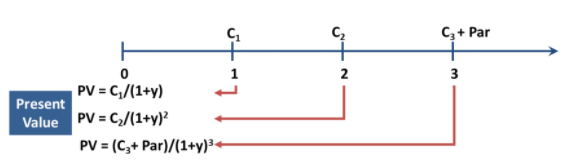

The market discount rate, also called the required yield or required rate of return, is the rate of return required by investors based on the risk of the investment. The present value of single cash flow can be calculated as follows:

The present value of a single cash flow can be calculated as follows:

$${ \text{Present value} }_{ t }=\frac {\text{Expected cash flow at time t}}{ { (1+i) }^{ t } } $$

Where:

Thus, the present value of a bond is simply:

$${ PV }_{ bond }=\frac { PMT }{ { (1+i) }^{ 1 } } +\frac { PMT }{ { (1+i) }^{ 2 } } +…+\frac { PMT + FV }{ { (1+i) }^{ n } } $$

Where:

For example, suppose that the coupon rate is 5% and the payment is made once a year for 5 years. If the market discount rate is 6%, the price of the bond is 95.788 for 100 of par value.

$$

\begin{array}{l|cccccc}

\text{Time Period} & 1 & 2 & 3 & 4 & 5 \\

\hline

\text{Calculation} & \frac { \$5 }{ { \left( 1+6\% \right) }^{ 1 } } & \frac { \$5 }{ { \left( 1+6\% \right) }^{ 2 } } & \frac { \$5 }{ { \left( 1+6\% \right) }^{ 3 } } & \frac { \$5 }{ { \left( 1+6\% \right) }^{ 4 } } & \frac { \$105 }{ { \left( 1+6\% \right) }^{ 5 } } \\

\hline

\text{Cash Flow} & \$4.717 & +\$4.450 & +\$4.198 & +\$3.960 & +\$78.462 & =\$95.788 \\

\end{array}

$$

In this example, the bond is trading at a discount as the price is below par value.

Note that the easiest way to do this calculation is with the help of the financial calculator (BA II plus) with the following input:

Now what if the coupon rate changed to 6%, paid annually, and the market discount rate still remains at 6%. Then, the price of the bond would be 100, and the bond would be trading at a par.

$${ PV }_{ bond }=\frac { 6 }{ { 1.06 }^{ 1 } } +\frac { 6 }{ { 1.06 }^{ 2 } } +\frac { 6 }{ { 1.06 }^{ 3 } } +\frac { 6 }{ { 1.06 }^{ 4 } } +\frac { 106 }{ { 1.06 }^{ 5 } } =100$$

If the bond happens to have a coupon rate of 7% and the market discount would still be 6%, its price would be 104.21, and it would be trading at a premium.

$${ PV }_{ bond }=\frac { 7 }{ { 1.06 }^{ 1 } } +\frac { 7 }{ { 1.06 }^{ 2 } } +\frac { 7 }{ { 1.06 }^{ 3 } } +\frac { 7 }{ { 1.06 }^{ 4 } } +\frac { 107 }{ { 1.06 }^{ 5 } } =104.21$$

As these examples demonstrate, the price of a fixed-rate bond, relative to par value, depends on the relationship between the coupon rate (Cr) and the market discount rate (Mdr). In summary:

Where :

Case 1: If C > Y: The bond trades at a premium

Case 2: If C < Y: Bond trades at a discount

Case 3: If C = Y: Bond trades at the par value

European bonds make annual payments, whereas Asian and North American bonds generally make semiannual payments. For semiannual payments, semiannual coupon payments are discounted by one half of the market discount rate (Mdr).

FRM Part 1 and Part 2 Complete Online Course

If the market price of a bond is known, the discounted cash flow equation can be used to calculate its yield-to-maturity or the internal rate of return of the cash flows. The yield-to-maturity is also the implied market discount rate.

The price of a fixed-rate bond will fluctuate whenever the market discount rate changes. When the market discount rate increases, the bond’s price decreases (inverse effect). Conversely, when the market discount rate decreases, the bond’s price increases (inverse effect).

However, the percentage price change is greater in absolute value when the market discount rate goes down than when it is up due to the convexity effect.

The sources of returns in bond valuation are coupons, reinvestment, and capital gain. If one of these sources decreases, the other one has to compensate.

Some examples of bonds are the plain vanilla bonds, zero-coupon bonds, and deferred coupon bonds, among others.

Suzanne Jennings purchased Bond A with a coupon payment per period of 4% for four years at $106. The bond’s yield is most likely:

The correct answer is A.

When the coupon rate is greater than the yield, the bond is priced at a premium above par value.

The present value of a newly issued 10-year, $1,000 par value security that will pay $60 every six months with an annual YTM of 8% is closest to:

The correct answer is B.

Or using the financial calculator:

N = 20; PMT = 60; FV= 1,000; I/Y = 4; CPT => PV = 1,271.81

All 3 Levels of the CFA Exam – Complete Course offered by AnalystPrep

Practice bond pricing, yield calculations, duration, and fixed income questions with CFA-style examples and mock exams.

Offered by AnalystPrep

Can You Really Pass the CFA Exam While Working Full Time? Are you... Read More

Attaining an FRM certification is vital in advancing your career in financial risks.... Read More

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.