Monitoring Alternative Investment Prog ...

Overall Investment Program Monitoring Investors enter alternative investment programs with specific goals: risk... Read More

To understand volatility skews and smiles, candidates must first grasp the concept of implied volatility and its limitations.

Implied volatility can be described as the outlook of a derivative contract’s expected standard deviation of returns. It is the degree and intensity to which derivative contracts are likely to persist.

The term “implied” in implied volatility refers to the market’s indications and expectations regarding future volatility. When using the Black-Scholes Merton Model (BSM) to calculate option prices, implied volatility is the parameter adjusted to make the calculated option price match the current market price. It acts as a “plug figure” to achieve this equilibrium.

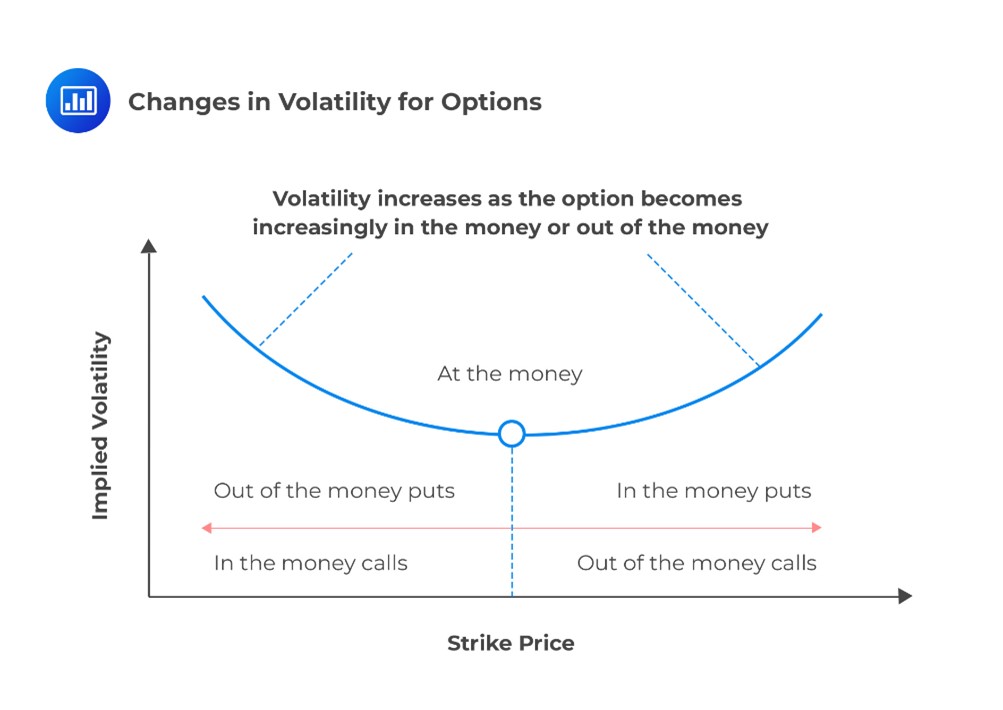

A criticism of the BSM is its assumption of a uniform volatility distribution across strike prices. In other words, it assumes that the volatility of an in-the-money put would be the same as that of an at-the-money option. However, as we will explore further, this assumption is not always valid in the financial markets.

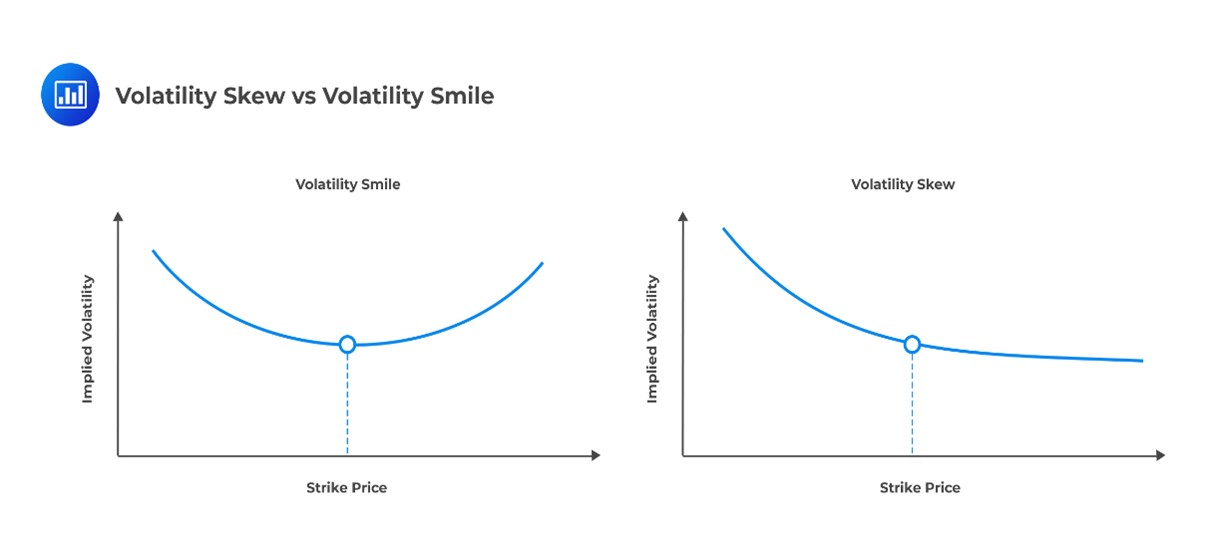

Volatility smiles are frequently observed in near-term equity options and currency options. They represent a departure from a flat volatility distribution, as both in-the-money and out-of-the-money options exhibit higher implied volatilities than at-the-money options.

Volatility skew refers to an asymmetric distribution of implied volatility across different strike prices. It creates a lopsided distribution, favoring either in-the-money or out-of-the-money options. In the example below, the blue line shows a skew with higher demand for in-the-money options. Skews are non-symmetrical and can vary in shape and intensity.

Implied volatility is not directly observable in the real world. It is derived by applying the BSM model to market prices and assuming that other variables can be estimated accurately. It is a supposition rather than a definitive value. Options prices in the real world can be influenced by various factors such as supply and demand. A volatility smile or skew indicates that the BSM model does not fully capture the dynamics of options prices.

Options traders seek skews and smiles to exploit mispriced volatility. These discrepancies can occur due to supply and demand dynamics. Traders aim to buy undervalued volatility or sell overpriced volatility in such situations.

Question

In the case of a volatility smile, implied volatility and prices for in-the-money options relative to at-the-money options are least likely to be?

- Higher.

- Lower.

- Over-priced.

Solution

The correct answer is A.

In a volatility smile scenario, implied volatility for in-the-money options is often higher than at-the-money options. This is because investors may be willing to pay more for the protection offered by in-the-money options in times of increased uncertainty.

B is incorrect. In a volatility smile scenario, implied volatility for in-the-money options is typically higher, not lower, compared to at-the-money options. This is because of the increased demand for downside protection in volatile markets.

C is incorrect. Market conditions and investor sentiment influence the prices of in-the-money options relative to at-the-money options. It’s not accurate to make a blanket statement that they are over-priced in all cases with a volatility smile.

Derivatives and Risk Management: Learning Module 1: Options Strategies; Los 1(h) Discuss volatility skew and smile

Offered by AnalystPrep

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.