Time Structure Models

Equilibrium Term Structure Models Equilibrium term structure models are built on theories about... Read More

The arbitrage-free framework is applied for credit analysis of a risky bond, assuming that interest rates are volatile. A binomial interest rate tree is constructed assuming no arbitrage. The tree is then verified if it has been correctly calibrated and used to value corporate bonds.

A fixed coupon corporate bond can be evaluated using the binomial interest rate tree in the following steps:

Consider a four-year zero-coupon corporate bond with a par value of $1,000 and a flat government bond yield curve at 5%. The risk-neutral probability of default (hazard rate) for each date of the bond is 2%, and the recovery rate is 40%.

Solution

$$ \begin{align*} \text{Value of the bond assuming no default (VND)} &= \frac{1000}{\left(1+0.05\right)^4} \\ & = 822.70 \end{align*} $$

Recall the calculation of CVA from a previous LOS.

$$ \begin{array}{c|c|c|c|c|c|c|c} \textbf{Year} & \textbf{EE} & \textbf{LGD} & \textbf{Hazard } & \textbf{PD} & \textbf{PS} & \textbf{EL} & \textbf{PV} \\ & & & \textbf{rate} & & & & \textbf{of} \\ & & & {} & & & & \textbf{EL} \\ \hline 1 & 863.84 & 518.30 & 2\% & 2.0000\% & 98.000\% & 10.37 & 9.8724 \\ \hline 2 & 907.03 & 544.22 & 2\% & 1.9600\% & 96.040\% & 10.67 & 9.6750 \\ \hline 3 & 952.38 & 571.43 & 2\% & 1.9208\% & 94.119\% & 10.98 & 9.4815 \\ \hline 4 & 1,000.00 & 600.00 & 2\% & 1.8824\% & 92.237\% & 11.29 & 9.2919 \\ \hline & & & & & & \textbf{CVA} & \bf{38.321} \end{array} $$

$$ \begin{align*} \text{Fair value} & =\text{VND} -\text{CVA} \\ & = 822.70 – 38.32 =$784.38 \end{align*} $$

YTM of the bond can be determined as the rate that solves the equation:

$$ \begin{align*} 784.38 & =\frac{1000}{\left(1+\text{YTM}\right)^4} \ \text{YTM} & = 6.26\% \end{align*} $$

$$ \begin{align*} \text{Credit spread} & = \text{YTM of the risky bond}\ – \text{Benchmark YTM} \\ & = 6.26\% – 5\% = 1.26\% \end{align*} $$

Thus, the compensation for credit risk received by the investor can be expressed in terms of:

In the previous example, we have determined the fair value and the credit spread of a risky bond, assuming a flat benchmark yield curve. This example will use the binomial interest rate tree to calculate the value of the bond assuming no default (VND) and the expected exposure in a volatile interest rate environment.

Given the spot rate curve for the annual payment benchmark Treasury, we can derive the discount factors and forward rates as per the following table:

$$ \begin{array}{c|c|c|c} \textbf{Maturity} & \textbf{Spot Rates} & \textbf{Discount Factors (DF)} & \textbf{Forward Rates} \\ \hline 1 & 4.00\% & 0.96154 & 4.000\% \\ \hline 2 & 5.00\% & 0.90703 & 6.010\% \\ \hline 3 & 6.00\% & 0.83962 & 8.029\% \end{array} $$

Using the above forward rates, an iterative process has been used to generate the following binomial tree, assuming an interest rate volatility of 15%.

$$ \begin{array}{ccc} \textbf{Time 0} & \textbf{Time 1} & \textbf{Time 2} \\ & & 10.69\% \\ & 6.89\% & \\ 4.000\% & & 7.86\% \\ & 5.12\% & \\ & & 5.90\% \end{array} $$

Consider a 5%, three-year corporate bond with a par value of $1,000. The risk-neutral probability of default for this bond has been estimated as 2%, and the recovery rate as 40%

We can determine the fair value of the bond as follows:

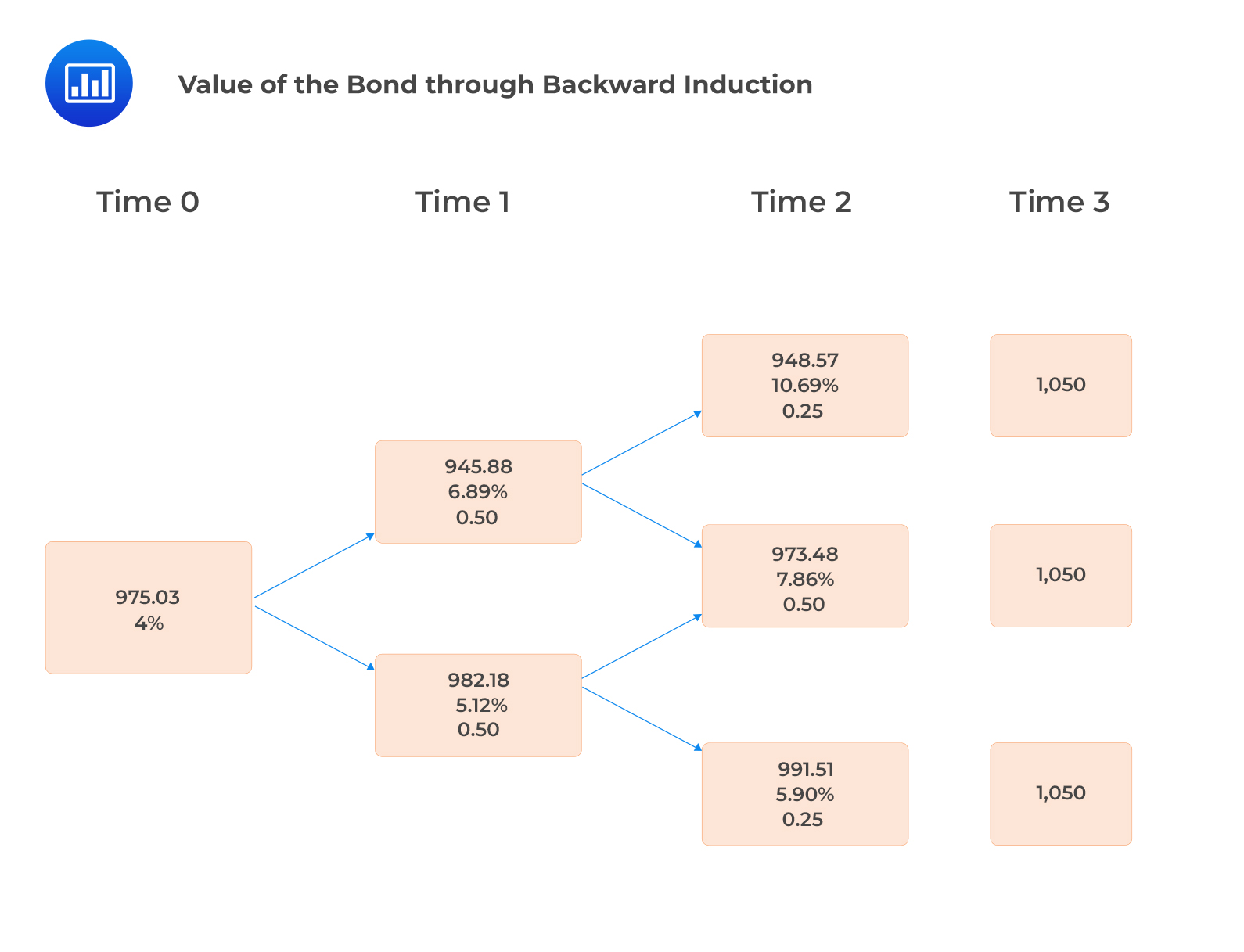

The first step is to determine the value of the bond, assuming no default (VND). This is done through backward induction.

N/B: The values in the above tree are subject to rounding errors

N/B: The values in the above tree are subject to rounding errors

Year 3 cashflows are the principal (1,000) plus the coupon of 50.

Year 2 values for the bond are obtained as follows:

$$ \begin{align*} \frac{1050}{1.1069} &=948.59 \\ \\ \frac{1050}{1.0786} &=973.48 \\ \frac{1050}{1.0590} & =991.50 \end{align*} $$

Year 1 values are obtained as follows:

$$ \begin{align*} \frac{1}{2}\times\frac{\left(948.59+50\right)+\left(973.48+50\right)}{1.0689} & =945.86 \\ \\ \frac{1}{2}\times\frac{\left(973.48+50\right)+\left(991.50+50\right)}{1.0512} &= 982.20 \end{align*} $$

Year 0 Value (VND) are obtained as follows:

$$ \frac{1}{2}\times\frac{\left(945.86+50\right)+\left(982.20+50\right)}{1.04}=975.03 $$

VND can also be determined by discounting the bond’s yearly cashflows at the relevant spot rates:

$$ VND =\frac{50}{1.04}+\frac{50}{\left(1.05\right)^2}+\frac{1,050}{\left(1.06\right)^3}=$975.03 $$

However, the binomial tree is key for calculating the expected exposure at each node when computing the CVA.

$$ \begin{align*} & \text{Expected exposure at each year} \\ & =\sum{\text{Value in node i at time t}\times \text{Probability}}+\text{Coupon for year t} \end{align*} $$

The next step is to calculate CVA.

$$ \begin{array}{c|c|c|c|c|c|c|c} \textbf{Year} & \textbf{EE} & \textbf{LGD} & \textbf{PD} & \textbf{PS} & \textbf{EL} & \textbf{Discount} & \textbf{PV of} \\ & & & & & & \textbf{Factors} & \textbf{EL} \\ \hline 1 & 1,014.03 & 608.42 & 2.000\% & 98.00\% & 12.17 & 0.9615 & 11.70 \\ \hline 2 & 1,021.76 & 613.05 & 1.960\% & 96.04\% & 12.02 & 0.9070 & 10.90 \\ \hline 3 & 1,050.00 & 630.00 & 1.921\% & 94.12\% & 12.10 & 0.8396 & 10.16 \\ \hline & & & & & & \textbf{CVA} & \bf{32.76} \end{array} $$

$$ \begin{align*} & {\text{Expected exposure for each year}} \\ & = \sum{\text{(Value at each node }}\times {\text{Probability}}) +{\text{Coupon}} \end{align*} $$

$$ \begin{align*} \text{Expected exposure for year one} & =\left(945.88\times0.5\right)+\left( 982.18\times0.50\right) \\ & +50 \\ & =1,014.03 \\ \text{Expected exposure for year two} & = (948.57\times0.25)+\left( 973.48\times0.5\right)\\ & +\left(991.51\times0.25\right) +50 \\ & =1,021.76 \\ \text{Expected exposure for year three} & = 1,050 \end{align*} $$

$$ \begin{align*} \text{Loss given default (LGD)} & = \left(1-\text{Recovery rate}\right)\times \text{Expected exposure} \\ LGD_1 & = 1,014.03\times\left(1-0.40\right)=608.42 \\ LGD_2 &= 1,021.76\times\left(1-0.40\right)=613.05 \\ LGD_3 &=1,050\times\left(1-0.40\right)=630.00 \end{align*} $$

The probability of default is calculated using the formula:

$$ PD_t=PS_{t-1}\times \text{Hazard rate} $$

Where:

$$ \begin{align*} \text{Probability of survival } (PS_t) &= 1- {\text{Cumulative conditional} \\ \text{probability of default}} \\ \text{Expected loss} & = LGD\times PD \\ \text{PV of expected loss} &=LGD\times\frac{PD}{\left(1+i\right)^t} \\ \end{align*} $$

CVA = sum of the present value of the expected loss for each period.

CVA = $32.76

VND = $975.03

$$ \begin{align*} \text{The fair value of the bond} & = VND\ – CVA \\ \text{Fair value}&= 975.03-32.76=$942.27 \end{align*} $$

Note that changes in the interest rate volatility have minimal effect on a corporate bond’s fair value. The volatility assumption has more weight on bonds with embedded options.

Similar to a fixed-coupon corporate bond, the arbitrage-free framework can also be used to analyze a floater as follows:

Question

A $1,000 par, 6% annual coupon corporate bond matures five years from today. The bond is currently priced with a credit spread of 150 bps over the benchmark par rate of 3%. The bond’s CVA is closest to:

- $43.63.

- $60.00.

- $1,084.86.

Solution

The correct answer is A.

$$ CVA = VND- \text{Price of risky bond} $$

VND is the value of the cash flows arising from the bond, discounted at the benchmark par rate

In this case,

$$ VND=\frac{60}{1.03}+\frac{60}{{1.03}^2}+\frac{1060}{{1.03}^3}=$1,084.86 $$

Price of the risky bond using credit spread = 3% benchmark rate + 1.5% = 4.5%. We will therefore discount the bond’s cash flows assuming a YTM of 4.5%

$$ \begin{align*} \text{Price of risky bond} &=\frac{60}{1.045}+\frac{60}{{1.045}^2}+\frac{1060}{{1.045}^3}=$1,041.23 \\ CVA &=$1,084.86-$1,041.23=$43.63 \end{align*} $$

Reading 31: Credit Analysis Models

LOS 31 (e) Calculate the value of a bond and its credit spread, given assumptions about the credit risk parameters.

Strengthen your understanding of risky bond valuation, credit valuation adjustment (CVA), yield to maturity, benchmark rates, and credit spread calculations with AnalystPrep’s CFA Level II practice resources.

Offered by AnalystPrep

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.