Components of the IPS

There is no standard format to the Investment Policy Statement, but most conform... Read More

A minimum-variance portfolio is the portfolio with the lowest possible risk for a given level of expected return. It is a key concept in Modern Portfolio Theory because it demonstrates how investors can reduce portfolio volatility through diversification rather than simply selecting the least risky individual assets.

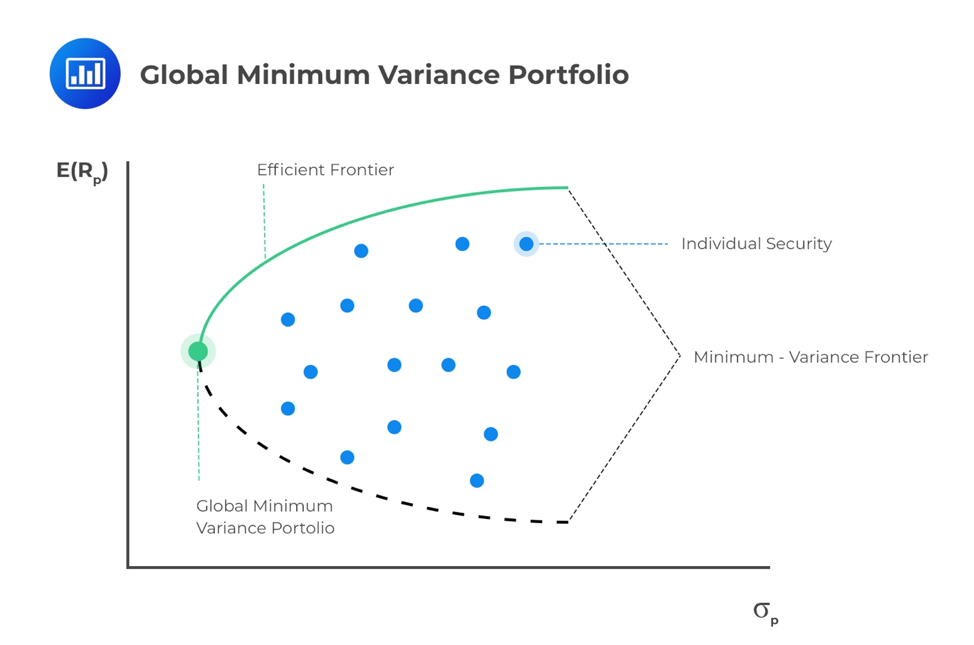

Minimum-variance portfolios form the minimum-variance frontier, while the portfolios that offer the highest expected return for each level of risk make up the efficient frontier.

In this study note, you’ll learn:

In theory, we could form a portfolio made up of all investable assets. However, this is not practical, and we must find a way to filter the investable universe. A risk-averse investor wants to find a combination of portfolio assets that minimizes risk for a given level of return.

When constructing a portfolio, it’s important to consider both the expected return and the level of risk involved. These portfolio characteristics depend on the assets included and how they interact with each other, which is measured through correlation. To explore various investment opportunities, we adjust the allocation to each asset. Different allocations create portfolios with distinct risk and return profiles. These profiles can be visually represented on a graph, with the expected return on one axis and the standard deviation on the other. This visualization helps investors make informed decisions about their portfolios.

For each level of return, the portfolio with the minimum risk will be selected by a risk-averse investor. This minimization of risk for each level of return creates a minimum-variance frontier – a collection of all the minimum-variance (minimum-standard deviation) portfolios. At a point along this minimum-variance frontier curve, there exists a minimum-variance portfolio that produces the highest returns per unit of risk.

Along the minimum-variance frontier, the left-most point is a portfolio with minimum variance when compared to all possible portfolios of risky assets. This is known as the global minimum-variance portfolio. An investor cannot hold a portfolio of risky (note: risk-free assets are excluded at this point) assets with a lower risk than the global minimum-variance portfolio.

The portion of the minimum-variance curve that lies above and to the right of the global minimum variance portfolio is known as the Markowitz efficient frontier. It contains all portfolios that rational, risk-averse investors would choose. We can also monitor the slope of the efficient frontier, the change in units of return per unit of risk. As we move to higher levels of risk, the resulting increase in return begins to diminish. The slope begins to flatten. This means we cannot achieve ever-increasing returns as we take on more risk, quite the opposite. Investors experience a diminishing increase in potential returns as portfolio risk increases.

| Minimum-Variance Frontier | Efficient Frontier |

| Includes every portfolio with minimum risk for a given return | Includes only the optimal portfolios that maximize return for each level of risk |

| Contains both efficient and inefficient portfolios | Contains only efficient portfolios |

| Includes the Global Minimum-Variance Portfolio | Begins at the Global Minimum-Variance Portfolio and extends upward |

| Used to identify the full opportunity set | Used by rational risk-averse investors for portfolio selection |

Suppose an investor can allocate funds between equities, government bonds, and real estate.

Rather than selecting the safest individual asset, the investor combines the three assets based on their expected returns, risks, and correlations.

The portfolio with the lowest overall standard deviation for a particular expected return is a minimum-variance portfolio. If it also provides the lowest risk among all risky portfolios, it is the global minimum-variance portfolio.

The global minimum-variance portfolio serves as the starting point of the efficient frontier.

Although it offers the lowest possible portfolio risk, it is not necessarily the portfolio that every investor should choose. Investors with higher return objectives typically move upward along the efficient frontier, accepting additional risk in exchange for higher expected returns.

This concept illustrates the trade-off between risk and return that underpins Modern Portfolio Theory. (CFA Institute)

Remember these relationships:

These distinctions are frequently tested in CFA Level I conceptual questions.

Question

Which statement best describes the global minimum-variance portfolio?

A. The global minimum variance portfolio gives investors the highest levels of returns.

B. The global minimum variance portfolio gives investors the lowest risk portfolio made up of risky assets.

C. The global minimum variance portfolio lies to the right of the efficient frontier.

Solution

The correct answer is B.

The global minimum variance portfolio lies to the far left of the efficient frontier. It is made up of a portfolio of risky assets that produces the minimum risk for an investor.

Minimum-Variance Portfolio — The portfolio with the lowest variance for a specified expected return.

Minimum-Variance Frontier — The set of portfolios that minimize risk for every level of expected return.

Global Minimum-Variance Portfolio — The portfolio with the lowest variance among all risky portfolios.

Efficient Frontier — The set of portfolios offering the highest expected return for each level of portfolio risk.

Portfolio Variance — A measure of the total variability of portfolio returns that depends on asset risk and correlations.

| Concept | Key Point |

| Minimum-Variance Portfolio | Lowest risk for a given expected return |

| Minimum-Variance Frontier | Collection of all minimum-risk portfolios |

| Global Minimum-Variance Portfolio | Lowest-risk portfolio of all risky assets |

| Efficient Frontier | Best return available for each level of risk |

| Portfolio Optimization | Balances expected return and portfolio risk |

A minimum-variance portfolio is the portfolio with the lowest possible risk for a given expected return.

The minimum-variance frontier includes every portfolio with the lowest risk for each expected return, while the efficient frontier includes only the portfolios offering the highest return for each level of risk.

It is the portfolio with the lowest variance among all risky portfolios.

Because they maximize expected return for every level of portfolio risk.

Not necessarily. Investors seeking higher expected returns may prefer portfolios farther along the efficient frontier, depending on their risk tolerance. (CFA Institute)

Work with minimum‑variance and efficient frontier problems, strengthen portfolio risk analysis, and build confidence for exam questions.

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.