When is the New 2021 CFA® Exam Window ...

At the beginning of 2021, the CFA Institute offered February 2021 level I... Read More

Portfolio management involves a trade-off between risk and return. Most amateur investors mistakenly focus only on the return aspect and lose sight of the risk taken to achieve the return. The portfolio performance measures are intended as metrics to compare different portfolios quickly. Like any financial ratio, these are not intended to be a one-stop answer to decide on a portfolio and should instead be used in conjunction with other data points.

The measure themselves are quite different from one another in the way that they measure the trade-off and how they define risk.

The Sharpe Ratio is defined as the portfolio risk premium divided by the portfolio risk:

$$ \begin{align} \text{Sharpe ratio} &= \frac{\text{Expected Return on the portfolio} – \text{Risk-free rate of interest}}{\text{Standard deviation of the portfolio}} \\ &= \frac{E(R_p) – R_f}{\sigma_p} \end{align} $$

The Sharpe ratio, or reward-to-variability ratio, is the slope of the capital allocation line (CAL). The greater the slope (higher number) the better the asset.

Note that the risk being used is the total risk of the portfolio, not its systematic risk, which is a limitation of the measure. The portfolio with the highest Sharpe ratio has the best performance, but the Sharpe ratio by itself is not informative. In order to rank portfolios, the Sharpe ratio for each portfolio must be computed.

A further limitation occurs when the numerators are negative. In this instance, the Sharpe ratio will be less negative for a riskier portfolio, resulting in incorrect rankings.

A client has three portfolio choices, each with the following characteristics:

Portfolio Statistics

$$\begin{array}{l|c|c|c}

& \textbf{Expected Return} & \textbf{Volatility} & \textbf{Beta} \\

\hline

\text{Portfolio A} & 15\% & 12\% & 10\% \\

\hline

\text{Portfolio B} & 18\% & 14\% & 11\% \\

\hline

\text{Portfolio C} & 12\% & 9\% & 5\% \\

\end{array}$$

The efficient market portfolio has an expected return of 20% and a standard deviation of 12%, and the risk-free rate of interest is 5%.

Based on the Sharpe ratio for each portfolio, the client should choose:

Solution

The correct answer is B.

\( \text{Sharpe ratio} = \frac{\text{Return on the portfolio} – \text{Risk-free rate of interest}}{\text{Standard deviation of the portfolio}} = \frac{R_p – R_f}{σ_p} \)

\(\text{Portfolio A’s Sharpe Ratio} = \frac{15\%−5\%}{12\%} = 0.83\)

\(\text{Portfolio B’s Sharpe Ratio} = \frac{18\%−5\%}{14\%} = 0.93\)

\(\text{Portfolio C Sharpe Ratio} = \frac{12\%−5\%}{9\%} = 0.77\)

The client should choose portfolio B as it gives the highest Sharpe ratio.

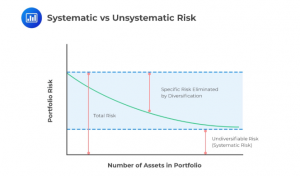

The Sharpe Ratio defines the risk in terms of standard deviation, which is a measure of total risk. Hence, it includes both systematic as well as unsystematic risk. The next measures that we look at – Treynor Ratio and Jensen’s Alpha – define the risk in a narrower way. In order to understand the applicability of the measure, we first need to understand the different types of risks.

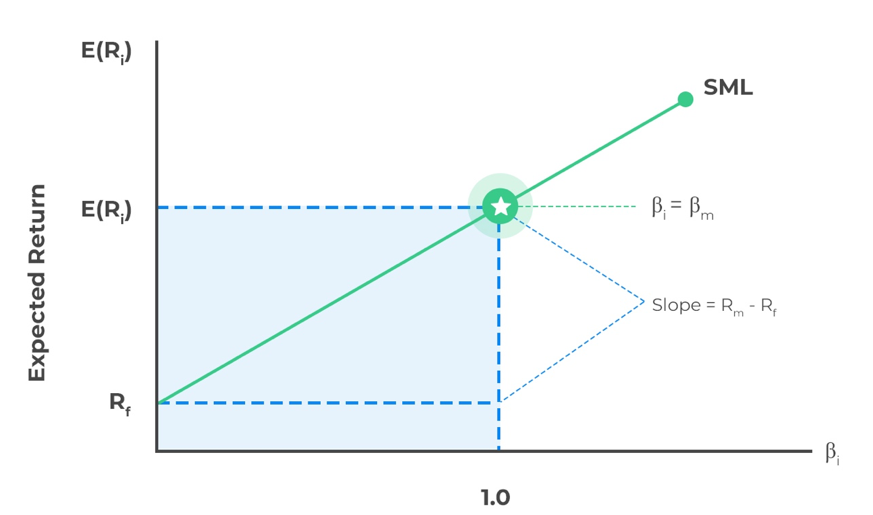

CAPM suggests that investors should hold the market portfolio and a risk-free asset. The true market portfolio consists of a large number of securities, and it may not be practical for an investor to own them all. Much of the non-systematic risk can be diversified away by holding 30 or more individual securities. However, these securities should be randomly selected from multiple asset classes. An index may serve as the best method of creating diversification.

It is important to note that only non-systematic risk can be eliminated through the addition of different securities into the portfolio. Systematic risk – the risk inherent to the entire market – cannot be diversified away.

The systematic risk of a portfolio is denoted by Beta:

$$\begin{align} \beta_i &= \frac{\text{Covariance between the security and the market returns}}{\text{Variance of the market return}}\\& = \frac{Cov(R_i, R_m)}{\sigma_m^2} \end{align}$$

Assume the risk-free rate is 2%, security has a correlation of 0.8 with the market index, and a standard deviation of 16%, while the standard deviation of the market is 12%. If the market expected return is 8%, the beta of the security is closest to:

Solution

The correct answer is B.

Recall that for a two-asset portfolio,

$$\text{Cov}(X, Y) = \rho_{X,Y} \times \sigma_X \times \sigma_Y$$

and since

$$\beta_i= \frac{Cov(R_i, R_m)}{\sigma_m^2} $$

then,

\(\beta_i= \frac{0.8 × 0.16\times 0.12}{0.12^2} = 1.07\)

Ready to take your FRM prep to the next level? Explore AnalystPrep’s Complete FRM Course and start mastering every concept with confidence.

The Treynor ratio is an extension of the Sharpe ratio that, instead of using total risk, uses beta or systematic risk in the denominator. As such, this is better suited to investors who hold diversified portfolios.

$$ \text{Treynor ratio} = \frac{\text{Expected return on the portfolio} – \text{Risk-free rate}}{\text{Beta of the portfolio}} = \frac{E(R_p) – R_f}{\beta_p} $$

As with the Sharpe ratio, the Treynor ratio requires positive numerators to give meaningful comparative results and, the Treynor ratio does not work for negative beta assets. Also, while both the Sharpe and Treynor ratios can rank portfolios, they do not provide information on whether the portfolios are better than the market portfolio or information about the degree of superiority of a higher ratio portfolio over a lower ratio portfolio.

A portfolio manager earned an average annual return of 12%. The beta of the portfolio is 0.9, and the volatility of returns is 25%. The average annual return for the market index was 14%, and the standard deviation of the market returns is 30%. The risk-free rate is 5%. Calculate the Treynor measure for the portfolio.

Solution

The correct answer is C.

Recall that,

$$ \begin{align} \text{Treynor Ratio} &= \frac{E(R_p) – R_f}{\beta_p} \\ &= \frac{12\% – 5\%}{9\%} = 7.8\% \end{align} $$

Jensen’s Alpha is based on systematic risk. The daily returns of the portfolio are regressed against the daily returns of the market in order to compute a measure of this systematic risk in the same manner as the CAPM. The difference between the actual return of the portfolio and the calculated or modeled risk-adjusted return is a measure of performance relative to the market.

$$ \text{Jensen’s alpha} = \alpha_p = R_p – [R_f + \beta_p (E(R_m)– R_f)]$$

If \(α_p\) is positive, the portfolio has outperformed the market, whereas a negative value indicates underperformance. The values of Alpha can also be used to rank portfolios or the managers of those portfolios, with the Alpha being a representation of the maximum an investor should pay for the active management of that portfolio.

Two portfolios have the following characteristics:

$$\begin{array}{c|c|c} \textbf{Portfolio} & \textbf{Return} & \textbf{Beta} \\ \hline A & 8\% & 0.7 \\ \hline B & 7\% & 1.1 \\ \end{array}$$

Given a market return of 10% and a risk-free rate of 4%, calculate Jensen’s Alpha for both portfolios and comment on which portfolio has performed better.

Solution

The correct answer is A.

$$ \text{Jensen’s alpha } ({ \alpha }_{ \text{p} })=R_p – [R_f + \beta_p (E(R_m)– R_f)] $$

\(\text{Jensen’s Alpha for Portfolio A} = 0.08 – [0.04 + 0.7(0.1 – 0.04)] = -0.002\)

\(\text{Jensen’s Alpha for Portfolio B} = 0.07 – [0.04 + 1.1(0.1 – 0.04)] = -0.036\)

Jensen’s Alpha is -0.2% and -3.6% for portfolios A and B, respectively. A higher Jensen’s Alpha (-0.2% in this case) indicates that a portfolio has performed better. Also note that both portfolio managers have been unable to create Alpha, but the manager of portfolio A has not been as bad as portfolio B’s manager.

Portfolio Performance Metrics

$$ \begin{array}{l|l|l|l} \textbf{Metric} & \textbf{What It} & \textbf{Formula} & \textbf{When to Use} \\ & \textbf{Measures} & & \\ \hline \text{Sharpe Ratio} & \text{Excess return per} & (R_p – R_f)/\sigma_p & \text{When comparing} \\ & \text{unit of total} & & \text{portfolios or} \\ & \text{risk (volatility)} & & \text{investments using} \\ & & & \text{total risk} \\ & & & \text{(standard deviation)} \\ \hline \text{Treynor Ratio} & \text{Excess return per} & (R_p – R_f)/\beta_p & \text{When portfolios} \\ & \text{unit of} & & \text{are well-} \\ & \text{systematic risk (beta)} & & \text{diversified and} \\ & & & \text{you want to} \\ & & & \text{isolate market risk} \\ \hline \text{Jensen’s Alpha} & \text{Abnormal return} & R_p – [R_f + & \text{To measure manager} \\ & \text{above CAPM-} & \beta_p (E(R_m) – R_f)] & \text{performance relative} \\ & \text{predicted return} & & \text{to expected market} \\ & & & \text{return} \\ \end{array} $$1. What is the difference between Sharpe and Treynor ratios?

The Sharpe Ratio evaluates returns per unit of total risk (standard deviation), while the Treynor Ratio focuses only on systematic risk (beta). Use Sharpe when assessing the absolute risk-adjusted return of a portfolio, and Treynor when comparing diversified portfolios relative to market risk.

2. How is Jensen’s Alpha calculated in CFA exams?

Jensen’s Alpha is calculated by subtracting the expected return (based on CAPM) from the actual return of a portfolio. Formula: $$ \text{Jensen’s alpha} = \alpha_p = R_p – [R_f + \beta_p (E(R_m)– R_f)]$$

Where \(R_p \) is the portfolio return, \(R_f\) is the risk-free rate, \(E(R_m\) is the expected market return, and \(\beta_p\) is the portfolio’s beta.

3. When should you use Sharpe vs Treynor?

Use Sharpe when evaluating portfolios that may include unsystematic risk (like actively managed funds). Use Treynor when comparing well-diversified portfolios where unsystematic risk is negligible. In short: Sharpe = total risk, Treynor = market risk only.

4. Are Sharpe and Treynor ratios tested in CFA Level 1 or 2?

Both Sharpe and Treynor ratios are introduced in CFA Level 1, particularly under Portfolio Management. However, deeper application and comparative analysis (including Jensen’s Alpha) are often emphasized more in CFA Level 2.

Sharpe, Treynor, and Jensen’s Alpha become easier when you apply them through timed questions and step-by-step solutions.

Strengthen your prep with AnalystPrep’s FRM study program featuring guided lessons, mock exams, and formula-based practice.

Learn Sharpe, Treynor, and alpha metrics with clear study tools.

Offered by AnalystPrep

At the beginning of 2021, the CFA Institute offered February 2021 level I... Read More

Let’s be honest for a moment. Most candidates walk out of the CFA... Read More

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.