Active Management

Active Management and Active Return Active management is a strategy employed by investors... Read More

Modeling risks and returns for alternative investments is challenging due to two key factors:

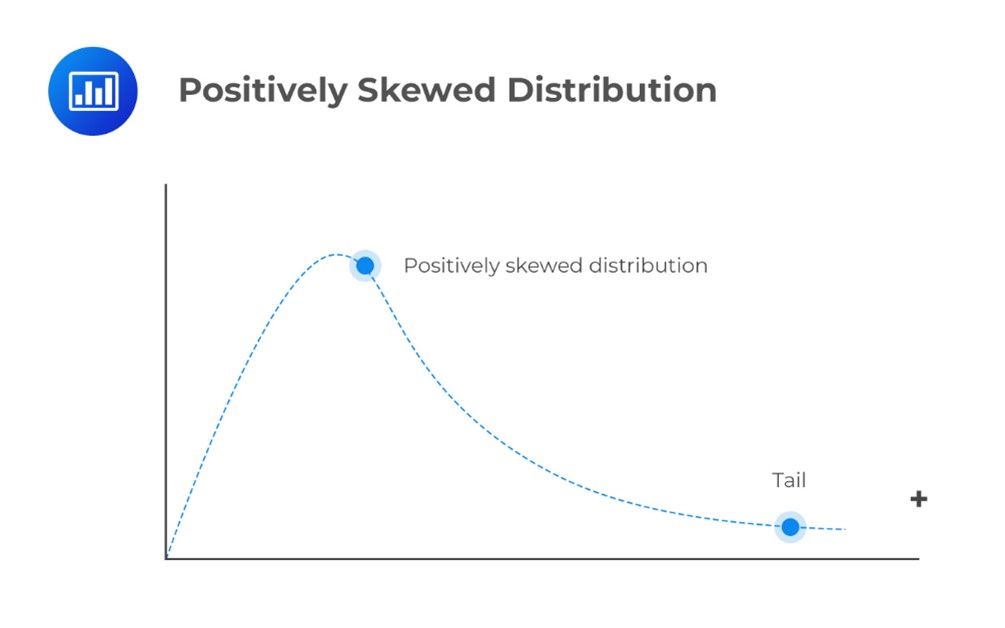

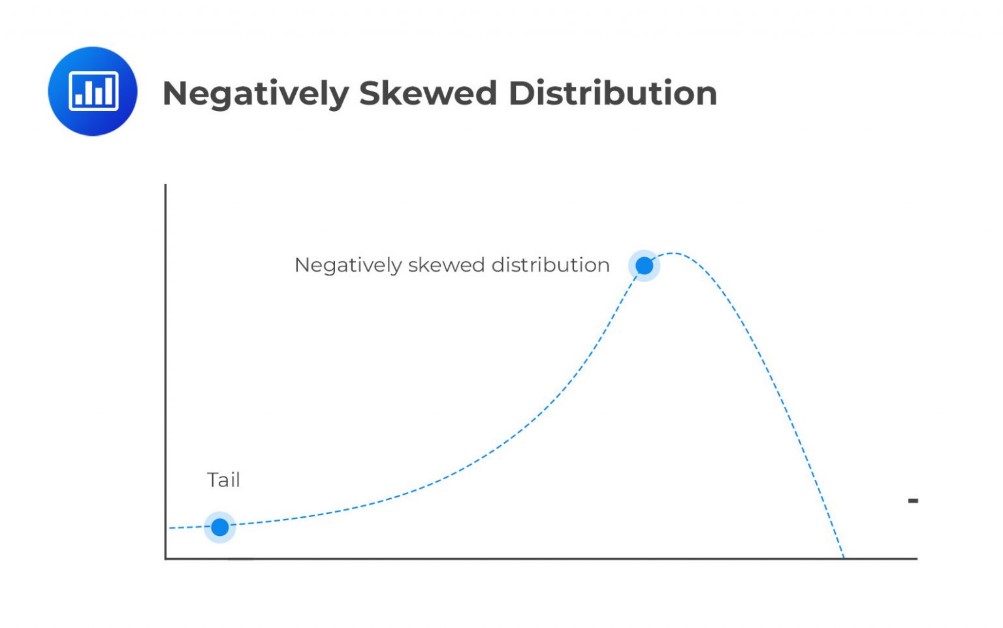

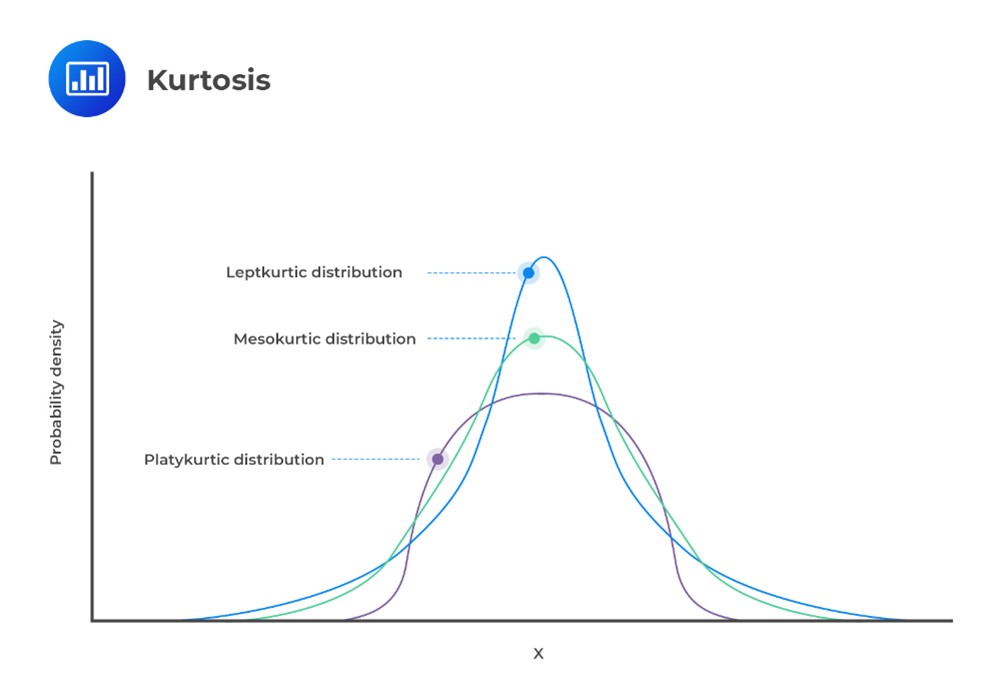

Candidates should understand that skewness and kurtosis in alternative assets make them behave differently from traditional assets. Modern Portfolio Theory (MPT) relies on normally distributed asset behavior, which is straightforward because all normal distributions look the same. But when skewness and kurtosis are introduced, it means the probabilities no longer fit this standard mold.

Asset allocators employ various approaches to address these challenges:

Monte Carlo Simulation involves generating numerous portfolio scenarios simulating different future outcomes. It’s like a statistical crystal ball. Parameters can be adjusted to match specific portfolio needs, and it doesn’t rely on the assumption of normally distributed returns.

Mean-variance optimization (MVO) can sometimes over-allocate alternative assets because it underestimates risk due to infrequent pricing and the assumption of normal returns. To correct this bias, practitioners set allocation limits. Approaches like mean-CVaR optimization consider downside risk and skewness, providing a more accurate asset allocation.

These approaches assign expected returns, risk, and correlations to different factors impacting asset returns, akin to Fama-French factor models. However, risk factors can vary depending on the investor, and correlations can change in dynamic market conditions. Some factors remain stable, while others fluctuate.

These methods help navigate the challenges of alternative asset allocation by considering non-normal asset behaviors and optimizing portfolios accordingly.

Question

Which of the following is least likely a common statistical impediment to performing traditional MVO on a portfolio of alternative investments:

- A bell curve.

- Excess kurtosis.

- Skewness.

Solution

The correct answer is A.

MVO is complex due to the diverse statistical distributions of returns seen in alternative investments. In modeling, we prefer a bell curve, representing a normal distribution, due to its known properties and probabilities.

B is incorrect. Kurtosis relates to the “height of the distribution.” In a normal distribution, most outcomes cluster around the center. But kurtosis means returns can concentrate elsewhere, more or less than expected.

These features add complexity to analyzing a portfolio of alternative investments.

C is incorrect. Skewness means the distribution is “off-centered,” like the Leaning Tower of Pisa. It’s an unhelpful property in statistical modeling.

Reading 28: Asset Allocation to Alternative Investments

Los 28 (f) Discuss approaches to asset allocation to alternative investments

Offered by AnalystPrep

Get Ahead on Your Study Prep This Cyber Monday! Save 35% on all CFA® and FRM® Unlimited Packages. Use code CYBERMONDAY at checkout. Offer ends Dec 1st.